By Tom Ramage

What Happened to U.S.-Korea Trade One Year After Tariffs

As exports to the U.S. fell in late 2025, shipments to China surged, suggesting market uncertainty will push Korea toward a more regionally focused economy.

Listen to this article

0:00 / 0:00

A year after President Donald Trump imposed double-digit tariffs on South Korea, the tariffs may be doing less to reduce deficits than to generate revenue. The bilateral goods trade deficit has only moderately budged down by 11.5 percent in 2025, and monthly exports have been too volatile to credit tariffs alone. As Korean exports to the United States dipped in the second half of 2025, exports to China surged, suggesting that uncertainty around the U.S. market may—inadvertently or otherwise—push Korea into becoming a more regionally oriented economy. But the tariffs themselves may not be the most consequential legacy of April 2. The distinction may belong to the associated USD 350 billion investment fund, which promises to deepen U.S.-Korea economic collaboration but whose outsized position could also strain Korea’s capital flows and the won. Future tariff threats may only exist to enforce this deal and keep these investments in place.

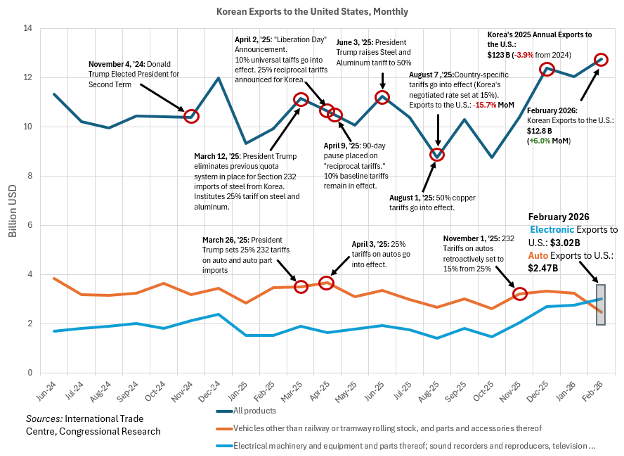

U.S. global trade has shifted considerably since Trump’s executive order on April 2, 2025, which invoked the International Emergency Economic Powers Act (IEEPA) to impose universal and “reciprocal” tariffs aimed at correcting trade deficits and reshoring U.S. manufacturing. Following temporary halts of reciprocal tariffs and negotiations, the Supreme Court struck down Trump’s tariffs in a 6–3 ruling earlier this year, reaffirming a 10 percent tariff authority to Section 122 tariffs for the time being (intended by the president to be 15 percent). Meanwhile, Section 232 tariffs on autos remain unaffected by the ruling, and anticipated tariffs against industries such as semiconductors are not yet in place (the president’s January proclamation on semiconductors does not appear to specifically target Korean companies).

A look back at the effects of these tariffs may show that it is difficult to discern the specific effects they had—universal, reciprocal, Section 232, or otherwise—on overall U.S.-Korea trade. A large, persistent U.S.-Korea trade deficit may reveal that they acted more as a revenue generator rather than a deficit eliminator. Apart from short-term fluctuations in exports, other effects may be seen in emerging trends in Korea’s trade with regional partners, including China.

According to the International Trade Centre, Korea’s trade surplus with the United States stood at USD 49.54 billion in 2025—an 11.5 percent reduction from the previous year. Its annual goods exports to the United States were down 3.9 percent in 2025, while its U.S. imports were up 1.7 percent from USD 72.5 to USD 73.7 billion—suggesting this was mostly due to weaker exports to the United States. Although the 11.5 percent annual deficit reduction may lend some weight to the tariffs’ favor, it is difficult to determine whether these reductions occurred solely because of the imposition of tariffs.

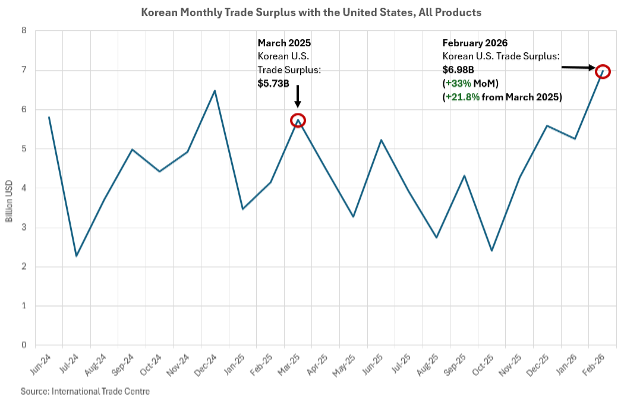

Korea’s monthly surplus with the United States shows something of a whipsaw effect. It fluctuated throughout the year after the announcement and initiation of the tariffs, and in February 2026, the most recent available data shows exports even increased by 21.8 percent in March 2025 from USD 5.73 billion to USD 6.9 billion. This could mean tariffs did not directly affect the U.S. trade deficit with Korea, as the IEEPA tariffs were intended to do.

With monthly exports (which were equally frantic), there were indeed some instances in which individual trade policy changes were correlated with changes in trade flows. But their numbers leveled off toward the end of the year, even higher than they were before the new Trump tariffs. In August, when the 15 percent tariff negotiated by the United States and Korea went into effect, U.S. exports were down 15.7 percent compared to the previous month. The imposition of Section 232 tariffs on autos may also have played a role in reducing their export values, as tariff-free electronics overtook autos in export value in February 2026—although this could also be explained by a surge in demand for data center equipment and AI infrastructure.

Along these lines, there was indeed a significant negative impact from auto tariffs, which had been in place since April 3 at 25 percent (subsequently lowered to 15 percent in November 2025) on Korean auto companies’ profits. These tariffs accounted for more than half of the United States’ tariff revenue in Q2 2025 alone. But rapid increases in overall exports in the months following tariff impositions, along with recent February export data showing monthly exports even higher than they were in March 2025 before the tariffs, show that trade remained too volatile to draw a definitive conclusion regarding Liberation Day’s direct effects on U.S. trade. Korean exports to the United States in February 2026 were 14.4 percent higher than they were in March 2025 (the month before Liberation Day was announced).

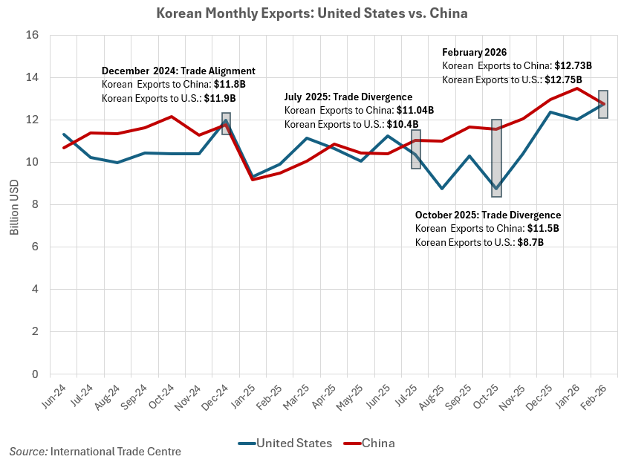

Instead of a wholesale reduction in the U.S.-Korea trade deficit, one concrete takeaway from Liberation Day may be that Korea is intensifying its level of exports to China. For example, Korea’s goods exports to the United States and China have been pacing closely for the past few years. In December 2024, Korea exported roughly similar amounts to both countries. Starting in July 2025, right before the imposition of negotiated tariffs on Korea, a divergence in Korea’s export value to the two countries emerged, peaking in October 2025, with exports to the United States at USD 8.7 billion and to China at USD 11.5 billion.

Korea’s exports to the United States have since rebounded, putting exports to China at roughly the same level, at USD 12.75 billion and USD 12.73 billion, respectively, in February 2026. The divergence once tariffs went into effect and the subsequent convergence following the U.S.-Korea trade deal suggest that tariffs on Korean goods in the U.S. market may have affected trade in this regard.

Whether the reorientation of Korean exports during H2 2025 was a direct result of tariffs or not, it nonetheless points toward a broader story of Korean regional integration. Seoul is making inroads toward liberalizing trade with Beijing and placing greater emphasis on assuming a role in regional blocs such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The complete recalibration of the United States as an export market, with a more permanent tariff regime in place, may push countries to diversify trade with other partners over the medium and long term.

Beyond this, if a permanent tariff regime were to remain in place, the evidence of the Korean trade surplus could cast the tariff’s primary responsibility as a revenue generator rather than a trade deficit eliminator. Gary Clyde Hufbauer and Ye Zhang from the Peterson Institute for International Economics (PIIE) estimate that in January 2026, U.S. tariff revenue from Korean goods stood at roughly USD 1.19 billion. This is a steep increase from the USD 27 million that the United States was collecting monthly from Korea in January 2025.

Should Korea’s exports to the United States persist under an extended regime (122, 301, 232, and otherwise), these tariffs may be factored into the long-term transactional cost of accessing the U.S. market. This would likely be similar to how they operated prior to the creation of the income tax, when tariffs provided most of the federal government’s revenue. In this future, economic theory, as viewed by the Trump administration, would likely be redefined within a new paradigm in which tariffs serve as an embedded feature—transcending the neo-classical model favored by the so-called “liberal international order.” With exports accounting for roughly 44.4 percent of Korea’s GDP, Korea’s scope for trade flexibility in this regard may be limited.

Still, the U.S. Court of International Trade (CIT) recently ruled that the Trump administration should refund all importers. The lack of any coherent narrative indicating broad-trend export reduction to the United States may indicate that it is too soon to tell how tariffs ultimately reroute trade from the United States. After all, it is up to the U.S. importer to administer the tariff payment, while the costs of the tariffs are shared along the value chain, which consists of suppliers, retailers, and consumers.

Instead, the greater impact of Liberation Day on Korea may not be the tariffs themselves, but rather the associated USD 350 billion investment fund’s impacts on the Korean economy. As the Council on Foreign Relations’ Senior Fellow Brad Setser’s research indicates, in 2025, Korea’s gross equity outflows nearly offset the inflows provided by the country’s current account surplus. At the same time, the Korean won has been weakening against the U.S. dollar, falling below KRW 1,500 to the dollar in March 2026 amid the war in Iran.

Concerns have emerged on how the outsized position of the USD 350 billion investment fund may exacerbate these dynamics by accelerating capital outflows and intensifying downward pressure on the won. The Bank of Korea maintains the ability to intervene, but its room for maneuver will ultimately be constrained by its foreign exchange reserves, which stood at USD 423.7 billion in March 2026. Moving past Liberation Day, all will likely be part of the policy challenges facing Korea’s central bank leaders, to be governed by former Bank for International Settlements economist Hyun Song Shin.

Accordingly, the real benchmark for assessing the impact of Liberation Day will likely be the effects of Korea’s tariff deal and the subsequent Korean investments in the United States—not only in terms of investment and job creation but also their broader implications for national accounts. Still, nothing is concrete until the expected USD 20 billion per year in investment commitments start rolling in and a long-term tariff regime is more securely in place.

Tom Ramage is Economic Policy Analyst at the Korea Economic Institute of America (KEI). The views expressed are the authors’ alone.

Feature image from The White House

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.