Search All Site Content

Total Index: 6946 publications.

Subscribe to our Mailing List!

Sign up for our mailing list to keep up to date on all the latest developments.

The Peninsula

South Korea’s Strategies to Cope With a Changing Global Trading System

The changing global trade environment poses challenges to South Korea’s export-driven economy. World trade has stagnated relative to world GDP in recent years, while global foreign direct investment (FDI) has declined. Although Korea’s exports of goods and services have fallen from 52 percent of GDP in 2012 to 44 percent in 2024, their share is well above the OECD average of 28 percent. Korea has become increasingly dependent on the United States as an export destination and on China as an important import source over the past fifteen years. Korea’s significant trade surplus with the United States and the concentration of its exports in key sectors leave it vulnerable to protectionist policies.

Trends in Korea’s Trade With China

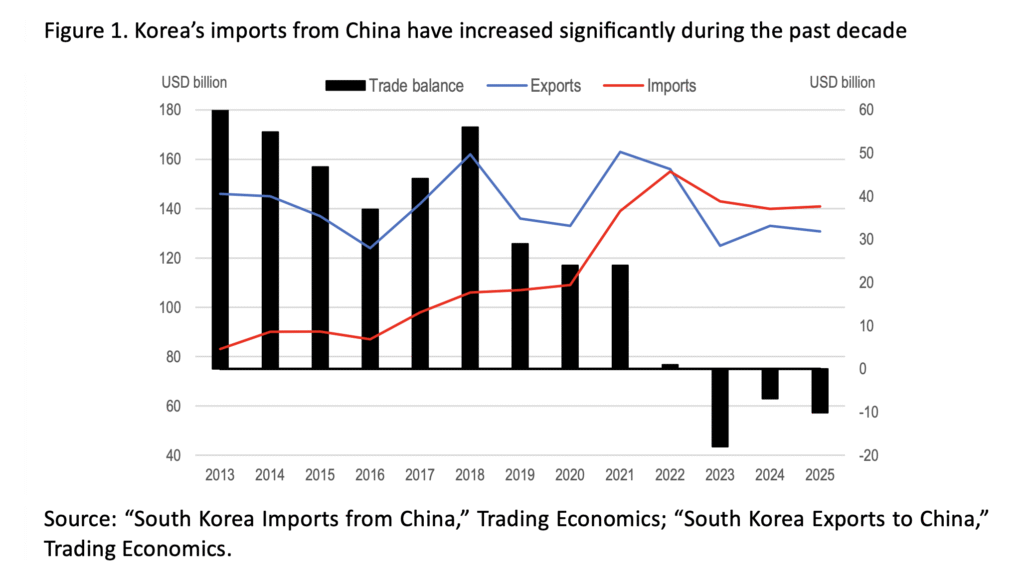

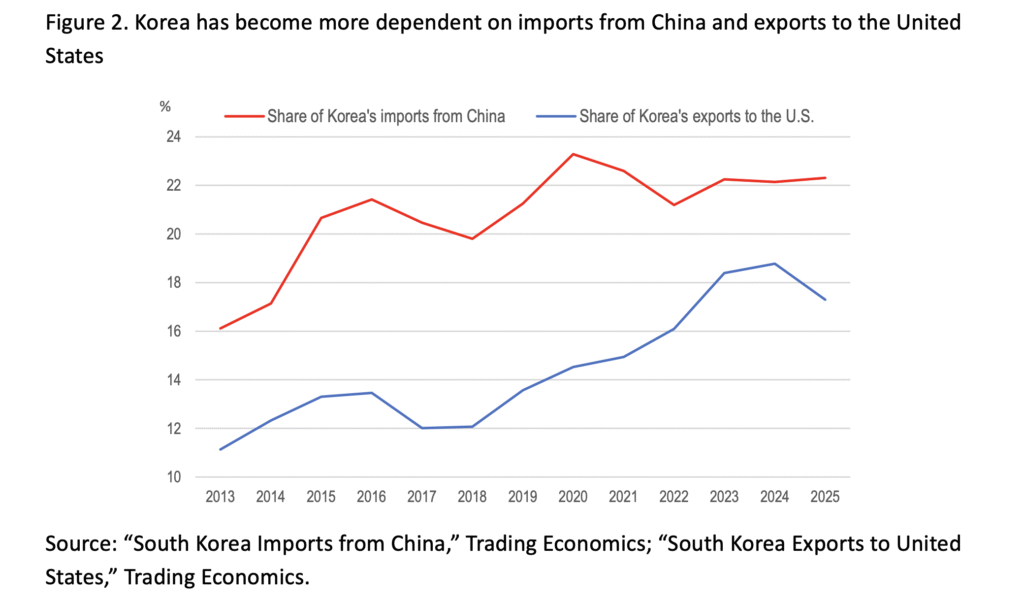

Korea’s imports from China surged from USD 83 billion in 2013 to USD 155 billion in 2022 before declining modestly over the past few years (Figure 1). China’s technological advancements and industrial policies have boosted its manufacturing competitiveness in many industries. In addition, the gradual reduction of Korea’s trade barriers under the 2015 Korea-China Free Trade Agreement (FTA) boosted Chinese exports to Korea. The impact of the FTA will continue to expand; by 2035, 85 percent of China’s exports to Korea will be duty-free, up from only 5 percent in 2015. Together, these factors helped boost China’s share of Korean imports from less than 16 percent in 2016 to 22 percent in 2025 (Figure 2), double the U.S. share.

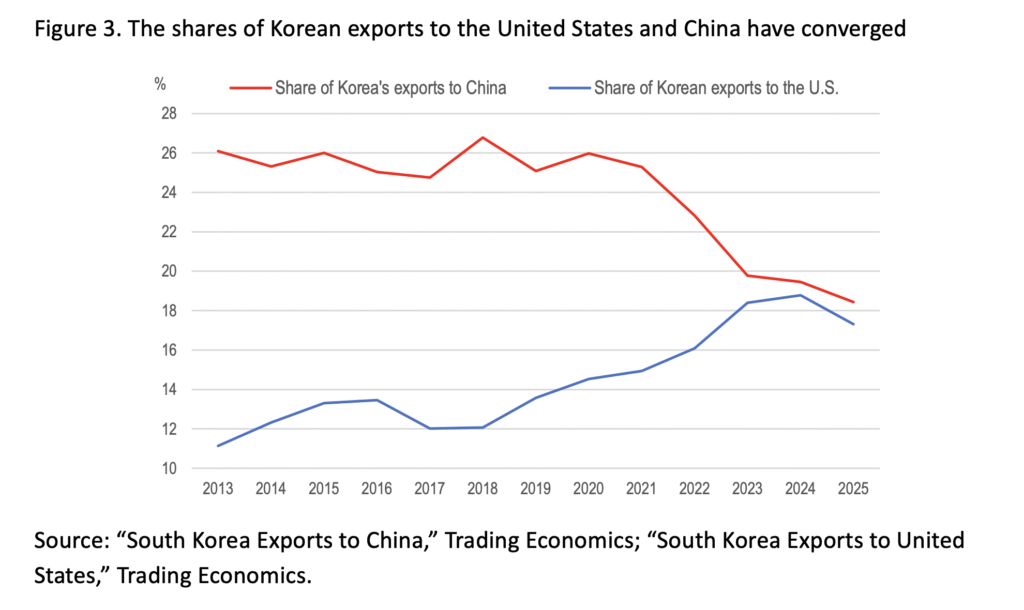

Korean exports to China, in contrast, have fluctuated over the past fifteen years without a clear upward trend (Figure 1). Consequently, China’s share of Korean exports fell from more than a quarter before the COVID-19 pandemic to 18.4 percent in 2025, converging with the U.S. share (Figure 3). China’s emphasis on developing local supply chains and enhancing its technological self-reliance under the 2020 Dual Circulation Strategy has slowed imports from Korea and other countries. Moreover, the Made in China 2025 initiative, launched in 2015, aimed to increase China’s domestic content of core materials to 40 percent by 2020 and 70 percent by 2025.

Around 80 percent of Korean exports to China consist of intermediate goods used for final production in China. A significant portion of these Chinese products is eventually shipped to the United States. As U.S. tariffs on Chinese imports increased during President Donald Trump’s first term, Chinese exports to the United States stagnated. One side effect was reduced Chinese demand for Korean intermediate goods. The Bank of Korea estimates that the 2018 U.S. tariff hikes on China reduced Korea’s exports to China and export-related production by approximately 3 percent.

U.S. restrictions on technology exports to China have created particular challenges for Korea’s semiconductor sector, which produces over 40 percent of its chips in China. Given these constraints, Korean semiconductor firms in China are unable to upgrade their facilities and produce more advanced chips. Consequently, their facilities in China risk becoming obsolete and losing competitiveness.

These challenges have contributed to Korea’s bilateral trade deficit with China during the past three years (Figure 1). Korea’s dependence on China for its manufacturing supply chains creates vulnerabilities for its economic security and global competitiveness.

Rising Korean Exports to the United States

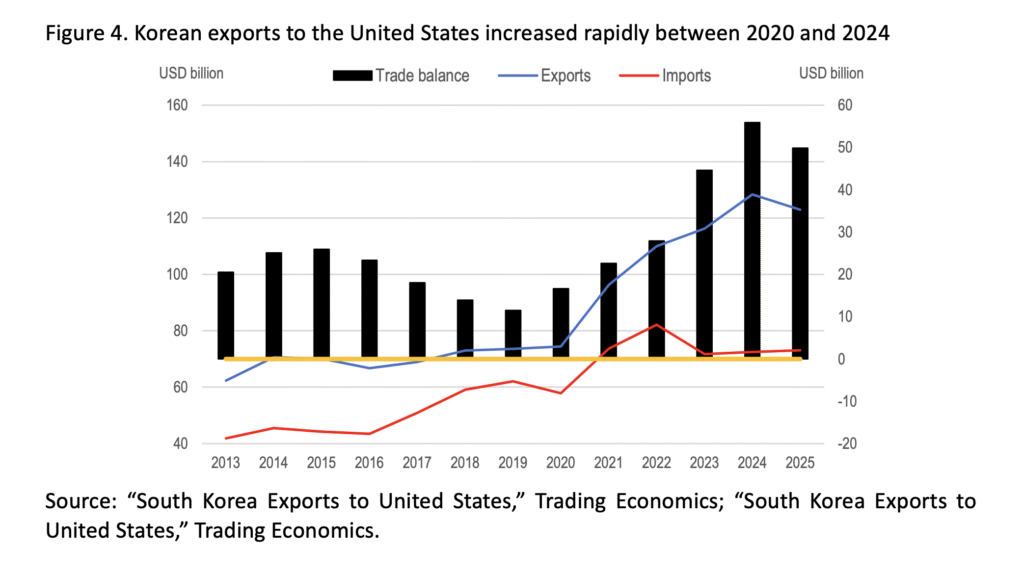

Korean exports to the United States have risen 73 percent from around USD 74 billion in 2020 to USD 128 billion in 2024 (Figure 4), driven by several factors. Perhaps most importantly, the rising competitiveness of Korean products has boosted sales. In addition, U.S. industrial policies, notably the Inflation Reduction Act and the CHIPS and Science Act of 2022, have attracted large investments in electric vehicles and batteries. The construction and expansion of manufacturing facilities in the United States by Korean firms have boosted demand for Korean capital goods, leading to a surge in exports.

The U.S. share of Korean exports rose to 18.8 percent in 2024, nearly matching China’s 19.5 percent share. Korea’s trade surplus with the United States reached a record high of USD 56 billion in 2024. Korea’s significant trade surplus with the United States and its concentration in key sectors such as semiconductors (around 20 percent of Korean exports), automobiles and parts (12 percent of exports), electronic equipment, and machinery and home appliances have contributed to protectionist pressures. FDI trends have followed similar patterns; Korea’s FDI flows to the United States have increased significantly compared to those to China.

Increasing Protectionist Pressures

In April 2025, the United States announced a 25 percent “reciprocal tariff” on Korean imports. After months of negotiations, the tariff was reduced to 15 percent following Korea’s pledge to invest USD 350 billion in the United States. However, tariffs on steel and aluminum remain much higher at 50 percent. In sum, the average tariff is much higher than the level set by the U.S.-Korea FTA, which eliminated virtually all tariffs on trade between the two countries in 2012. The tariffs probably played a role in the decline in Korean exports to the United States in 2025 and the USD 6 billion drop in Korea’s bilateral trade surplus with the United States.

However, despite the higher tariffs and the ongoing war in the Middle East, Korea’s exports to the United States increased 47.1 percent in March 2026 (year-on-year), led by shipments of semiconductors. It is difficult to identify the specific effects of President Trump’s tariffs, including the universal, reciprocal, Section 232, or other tariffs, on overall U.S.-Korea trade.

More protectionist pressures may be in the pipeline. U.S. tariff rates on semiconductors, which have been subject to a Section 232 investigation (national security considerations), have not been decided. In March 2026, the United States launched a Section 301 (foreign trade practices deemed unfair or harmful to the United States) investigation of Korea, as well as fifteen other countries and the European Union. It focuses on the rather vague issue of “structural excess capacity in manufacturing.” This was followed by a Section 301(b) investigation into whether Korea and fifty-nine other countries have failed to impose and effectively enforce prohibitions on imports of goods produced with forced labor.

A Strategy for Korea to Cope With Protectionist Pressures

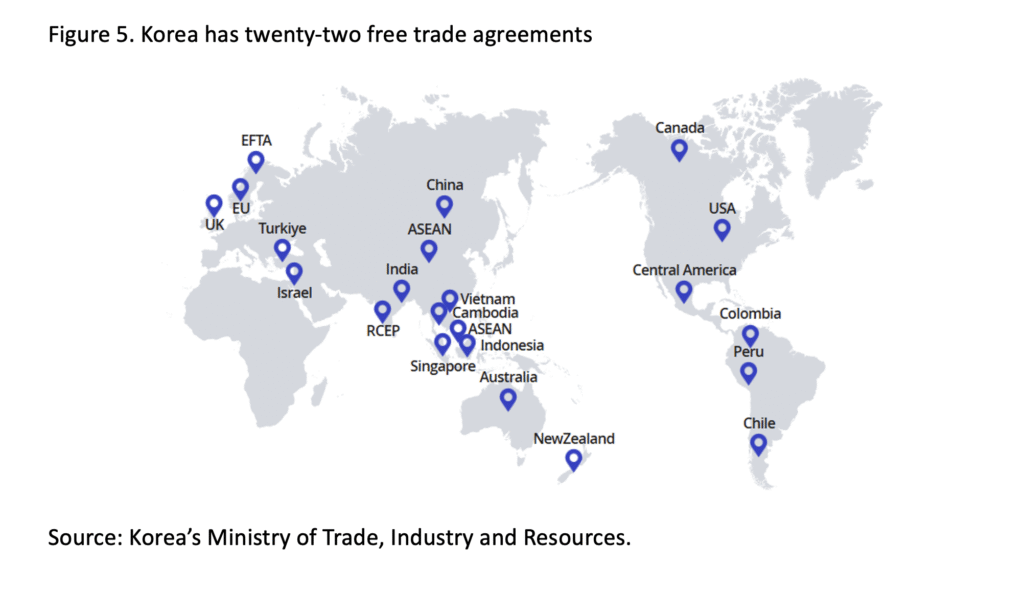

Korea has made extensive efforts to diversify its trading partners since negotiating its first FTA with Chile in 2003. It now has twenty-two free trade agreements covering fifty-nine countries (Figure 4), accounting for 85 percent of global GDP (Figure 5). Given the extensive coverage, the gains from additional FTAs may appear to be modest.

Two policies would enhance Korea’s trade prospects. First, improving existing FTAs would increase their benefits. The higher the level of openness created by a trade agreement, the greater the trade-creation effect and the lower the trade-diversion effect, which occurs when a country shifts its imports from a more efficient external producer to a less efficient producer within the FTA. This results in higher costs for consumers and a net economic loss. Second, Korea could negotiate new FTAs with emerging markets. In 2024, the government announced its aim to increase the number of FTAs to seventy-six countries, accounting for 90 percent of global GDP. If achieved, Korea would surpass Singapore, currently the highest at 87 percent. The government identified seven emerging countries—Kenya, Tanzania, Morocco, Thailand, Pakistan, Serbia, and the Dominican Republic—as potential partners for FTAs.

Korea’s top trade priority should be to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), the world’s fourth-largest FTA in terms of GDP, after the U.S.-Mexico-Canada Agreement, the European single market, and the Regional Comprehensive Economic Partnership (fifteen countries in the Asia-Pacific region). The CPTPP, which includes two important countries that do not have an FTA with Korea (Japan and Mexico), is widely considered the “gold standard of FTAs” and the most comprehensive, with thirty chapters. The CPTPP’s commitment to a rules-based order and economic integration is crucial amid the faltering world trade system.

Korea considered joining the CPTPP in 2021 under the Moon Jae-in administration and again under the Yoon Suk Yeol administration. However, one obstacle to joining the CPTPP is concerns about its impact on the agricultural sector. Nevertheless, Minister of Trade Yeo Han-koo stated, “It’s time to diversify our export markets and begin strategic reviews of agreements like the CPTPP in the midst of intensifying U.S.-China trade tensions.” The Lee Jae Myung administration has repeatedly expressed interest in joining the CPTPP and said that a potential membership in the trade alliance is under review.

Randall S. Jones is a Distinguished Fellow at the Korea Economic Institute of America (KEI). The views expressed are the authors’ alone.

Feature image from Shutterstock.

This material is distributed by KEI on behalf of the Korea Institute for International Economic Policy. Additional information is available at the Department of Justice, Washington, DC.