Understanding the $350 Billion MOU Putting Seoul Under Pressure

The deal may not only help Korea avoid higher tariffs, but also lower the cost of capital for strategic investments in the United States.

South Korea faces a consequential decision regarding its USD 350 billion investment memorandum of understanding (MOU) with the United States. Under the agreement, Washington selects investment projects while Seoul provides the funding. After these break even, 90 percent of returns will flow to the United States. Korea, in turn, gains a measure of relief from wide-sweeping and industry-specific tariffs, including the important automobile industry. The MOU is not a legal treaty and is instead enforced by the threat of tariffs, a mechanism that could extend beyond trade to other areas of bilateral tension.

While the MOU was made prior to the Supreme Court ruling against the use of the International Emergency Economic Powers Act (IEEPA) to authorize tariffs, the Donald Trump administration is already implementing alternative paths to reestablish tariffs and maintain its leverage. A special funding bill required to operationalize the agreement remains up for vote in the National Assembly, and with the White House pressing for faster action ahead of its November midterm elections and the first Japanese MOU investments recently announced, Korea may have to decide whether to move forward on U.S. terms or risk inviting the very tariff pressure the MOU was designed to avoid.

The investment MOU from the finalized trade and investment deal, released in November, has reemerged amid Trump’s threat of 25 percent tariffs on Korea. In a social media post on January 26, Trump questioned why Korea has not passed the MOU or the necessary bill to start funding investment projects in the United States. This comes as net approval rates for the U.S. president are falling and ahead of the midterm elections in November.

The MOU recognizes Korean investment commitments in sectors that help advance U.S. economic and national security interests, including energy, semiconductors, pharmaceuticals, critical minerals, AI, and quantum computing. Shipbuilding is in this group as well and is slated to receive USD 150 billion from the USD 350 billion package.

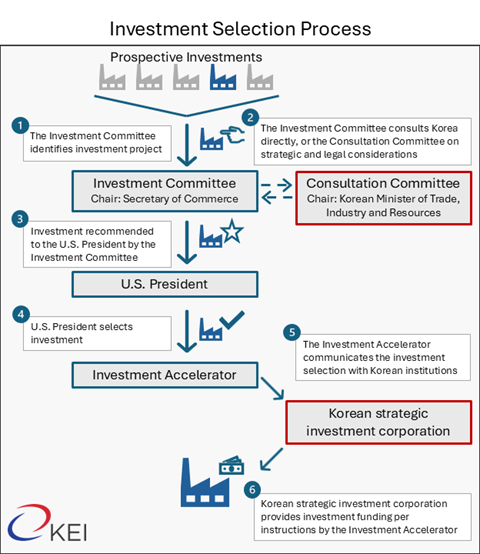

Per the MOU, Trump will select investments that are recommended and deemed commercially reasonable by an investment committee established by the president and chaired by the U.S. secretary of commerce. Prior to making any recommendations, the investment committee will consult a consultation committee chaired by Korea’s Minister of Trade, Industry and Resources to consider their strategic and legal aspects. Once the president selects an investment, Korea will provide funding in separate tranches, with forty-five days to meet funding requirements and dollar-denominated funds immediately accessible by the U.S. Investment Accelerator. Korea retains the right to decline any selected investment, but doing so invites a targeted tariff response, the scope of which remains at the president’s discretion.

Following concerns from the Lee Jae Myung administration that large investment outflows under the agreement could weaken the won internationally, the MOU includes a USD 20 billion annual cap on investment flows. All USD 350 billion in investments must be announced during Trump’s term, but for Korea, the annual funding cap marks an important addition compared to the terms in the U.S.-Japan MOU, which require full funding before the end of Trump’s term.

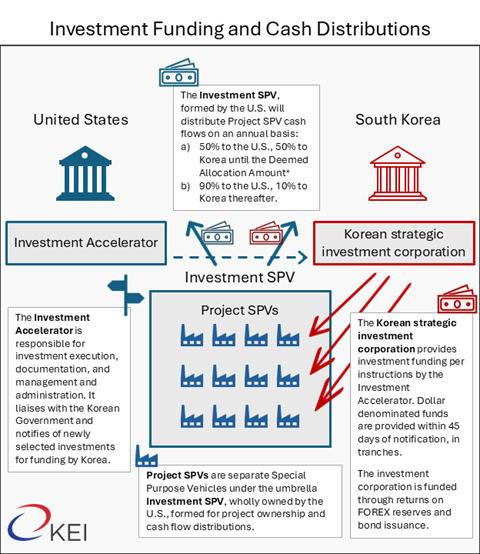

Investment funds and free cash flows from investments will be handled through a special purpose vehicle (SPV) owned and operated by the United States. An umbrella investment SPV will receive funding from Korea and distribute it to approved projects, each of which will be held under its own project SPV. Free cash flows will be paid by each project SPV to the investment SPV, distributed annually in equal shares to both governments until the cost of investment has recouped, after which 90 percent will be allocated to the United States and the remaining 10 percent to Korea.* Should Korea decline to fund a selected investment, it forfeits its share of free cash flows until the United States receives the full amount it would have otherwise received.

A section of the MOU intends to facilitate investments in the United States. It states that Washington will arrange leases for federal land, secure access to water and energy, and expedite any applicable regulatory processes for investment projects, subject to feasibility and legal constraints.

While the MOU states that the United States owns the project SPVs, it establishes a preference for Korean management and suppliers. Firstly, the United States will select a manager for each project suggested by Korea, whenever feasible. Secondly, the Korean government may recommend Korean vendors and suppliers over other foreign competitors.

Accordingly, Korea intends to fund the investment SPV by establishing a strategic investment corporation, operated as a fund for up to twenty years, pending National Assembly approval. The corporation will be funded through returns generated from Korean foreign exchange reserves—managed by the Bank of Korea and currently sitting at roughly USD 428.1 billion—and by issuing government-guaranteed bonds.

Notably, Trump’s frustration with the pace of the investment rollouts stems from political gridlock in Seoul. The ruling Democratic Party has argued that the MOU does not require legislative ratification, while the opposition People Power Party has contended that it does. As of March 4, the parties have agreed to move the special funding bill and enable the MOU investments for a vote in the National Assembly on March 12. Nonetheless, the Lee administration has stated that Korea will begin preliminary reviews of potential U.S. investment projects, suggesting that the MOU plans are still moving forward.

The Full Picture

The MOU effectively authorizes the Trump administration to pick investment projects for Korean funding, and Korea will be reluctant to disagree with these picks due to the threat of higher tariffs. Korea may recoup the investment amounts, subject to project-specific risks—the majority of returns will be kept in the United States. Korea bears the financial risk of defaulting on projects but cannot freely reject risky investments under the threat of reimposed tariffs. This creates a potential moral hazard where the United States is incentivized to select riskier, higher-reward deals at Korea’s expense. Apart from the USD 20 billion annual funding cap, these terms are similar to those found in the U.S.-Japan MOU.

The MOU may not only help Korea avoid higher tariffs, but also effectively lower the cost of capital for strategic investments in the United States, creating opportunities for Korean companies and helping to subsidize a long-term economic relationship. But it is also important to consider that each project will be owned by the United States, not by Korean companies, which will receive only preferential treatment. There is no guarantee of Korean involvement after the Korean side funds a project. For example, the diamond grit facility announced as part of the first tranche of Japanese MOU investments will be led by De Beers Group’s subsidiary Element Six—not a Japanese firm. This raises the question of what incentives are in place to attract Korean corporations that are expected to contribute unique know-how and expertise. Trump, meanwhile, has clear incentives to move quickly, with significant investment announcements likely to feature prominently in his pitch ahead of the midterms.

In the interim, U.S.-Korea cooperation in the strategic industries listed in the MOU appears to be making headway, even without explicit institutional backing from the investment fund. New projects, such as the USD 7.4 billion U.S. critical mineral smelter project in Tennessee involving Korea Zinc, operate under an SPV-style structure, possibly paving the way for investment funds to be distributed through existing channels. Notably, another early Japanese MOU investment of USD 2 billion benefits a preexisting offshore project, GulfLink, signaling that MOU funds may benefit some projects already underway. As the United States looks with increasing urgency to create new investments ahead of the November elections, more projects could be announced with the SPV legal structure in mind, potentially positioned to receive MOU funding once supporting structures are established, without waiting for the ratification process in the National Assembly.

There is also a broader caveat that the MOU is not legally binding. Rather, it is enforced by the threat of tariffs and may not prevent the United States from imposing new, possibly ad hoc tariffs to create leverage in other emerging issues, such as defense cost-sharing or digital trade. While the recent Supreme Court ruling struck down IEEPA tariffs, the use of Section 232 tariffs on key Korean exports and the potential use of other presidential tariff authorities keep Seoul under pressure to advance the MOU as quickly as possible.

Nils Wollesen Osterberg is Economic Policy Associate at the Korea Economic Institute of America. The views expressed here are the author’s alone.

Feature image from the U.S. Department of Energy.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.

* Distributions will be shared equally between the United States and South Korea until a “Deemed Allocation Amount” has been distributed to each, after which 90 percent of distributions will be allocated to the United States and ten percent to South Korea.

Deemed Allocation Amount with respect to an Investment means an amount equal to the sum of:

- the product of:

- the Deemed Interest Rate as of the date on which such Investment was funded by Korea and

- the Investment Amount less prior distributions pursuant to clause (B) below in respect of such Investment (but in no event less than zero) plus the Interest Carryover Amount;

- the Investment Amount divided by the lesser of (x) the anticipated life of the project underlying such Investment (as expressed as a number of years) as determined in good faith by the United States upon consultation with Korea and (y) 20; and

- any Carryover Amount.