How South Korea Is Trying to Increase Its Supply-Chain Resilience

South Korea should enhance its supply-chain resilience in response to trade disruptions amid a changing world order.

South Korea has become more dependent on China for imports and on the United States for exports. This concentration of trade with the two global superpowers poses risks for Korea. Protectionist policies by the United States have disrupted the global trading system, creating increased vulnerability and uncertainty for Korea’s trade-dependent economy. In addition, supply-chain issues have posed a recurring challenge for Korea, reflecting its heavy reliance on certain countries for key inputs. To cope with the changing world order, Korea needs to enhance its supply-chain resilience.

Global economic integration and openness have created highly efficient and profitable supply chains that are potentially fragile, as disruptions to Korea’s trade in recent years have shown. In July 2019, Japan imposed controls on fluorinated polyimide, photoresist, and hydrogen fluoride—all critical inputs for semiconductor production. In November 2021, China halted exports of urea, a crucial ingredient for diesel-powered vehicles. The 2022 Russian invasion of Ukraine disrupted Korea’s imports of rare gases that are also essential for semiconductors. Ukraine accounted for 23 percent of Korea’s neon imports, 31 percent of krypton, and 18 percent of xenon. And in 2023, China tightened export controls on gallium, germanium, and graphite—critical minerals central to advanced electronics, renewables, telecommunications, and defense.

The war in the Middle East poses additional supply chain concerns. Samsung Electronics and SK Hynix, the world’s largest makers of memory semiconductor chips, rely on Qatar for 65 percent of their helium imports, which are used to cool the chips during production. Qatar halted helium production shortly after the war began. Helium is just one of fourteen semiconductor supply-chain materials that the Korean government has flagged for monitoring due to its heavy vulnerability to the ongoing war.

Export Restrictions Are Surging

Most manufactured products include metals and minerals. A mobile phone, for example, contains up to fifty metals and minerals. While demand for critical raw materials is rising rapidly, supply has adjusted more slowly. Moreover, the extraction and processing of these are highly geographically concentrated; for example, the top three countries for cobalt, lithium, and nickel account for over two-thirds of global production, and nearly 90 percent for rare-earth elements. The high ownership concentration has prompted some governments to use export restrictions to pursue various objectives, such as promoting domestic processing, protecting local downstream industries, safeguarding domestic supply, and protecting the environment.

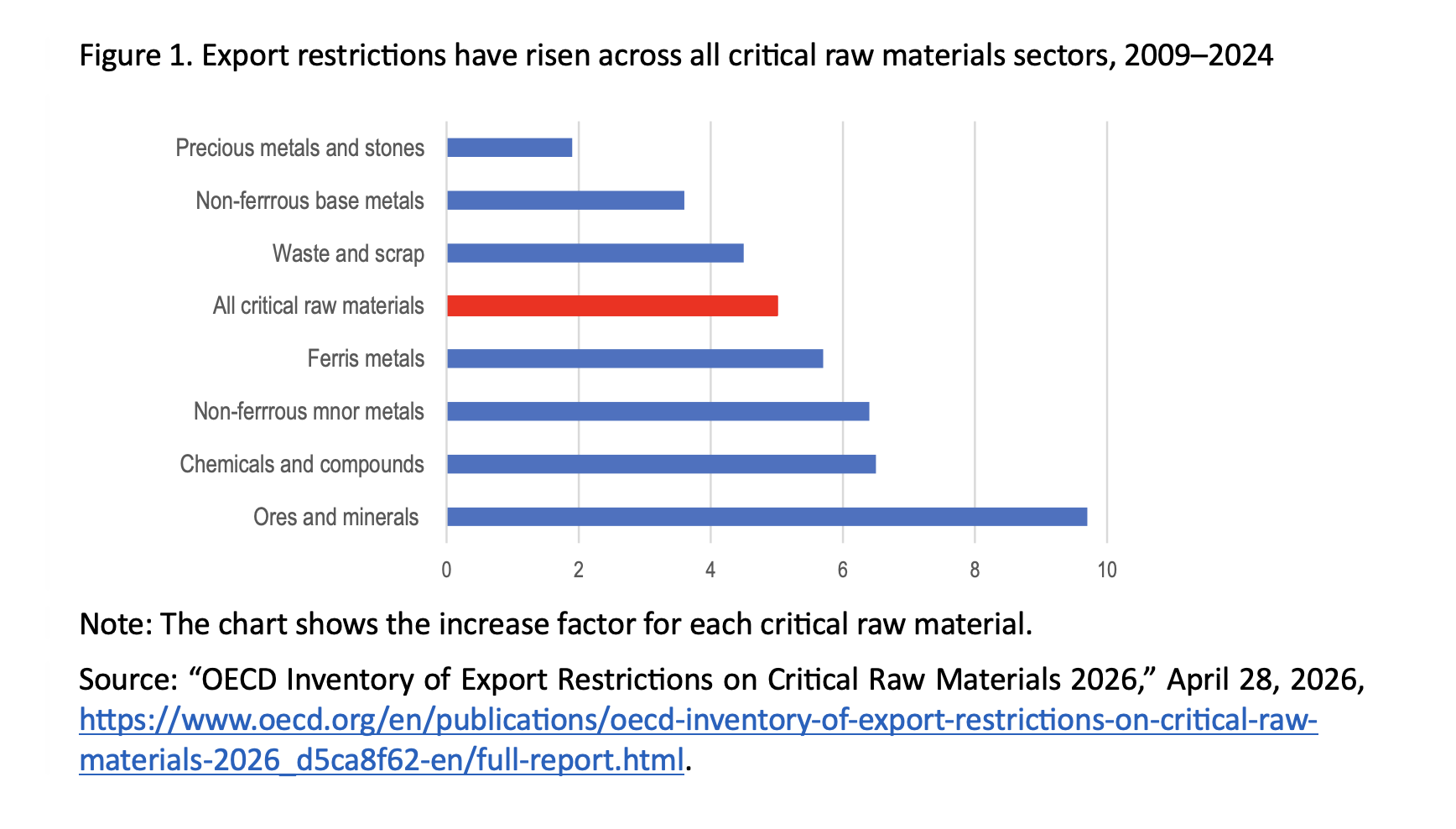

Export restrictions on critical raw materials have increased fivefold since 2009, according to a recent OECD study. The restrictions have risen across all critical raw material sectors, with the largest increases in ores and minerals and chemicals and compounds (Figure 1). Many of the restrictions apply to materials critical to supply chains central to energy and digital transitions and to defense. For example, around 70 percent of global exports of cobalt and manganese were subject to at least one export restriction between 2022 and 2024. The share is also high for graphite (47 percent), rare-earth elements (45 percent), and tin (41 percent).

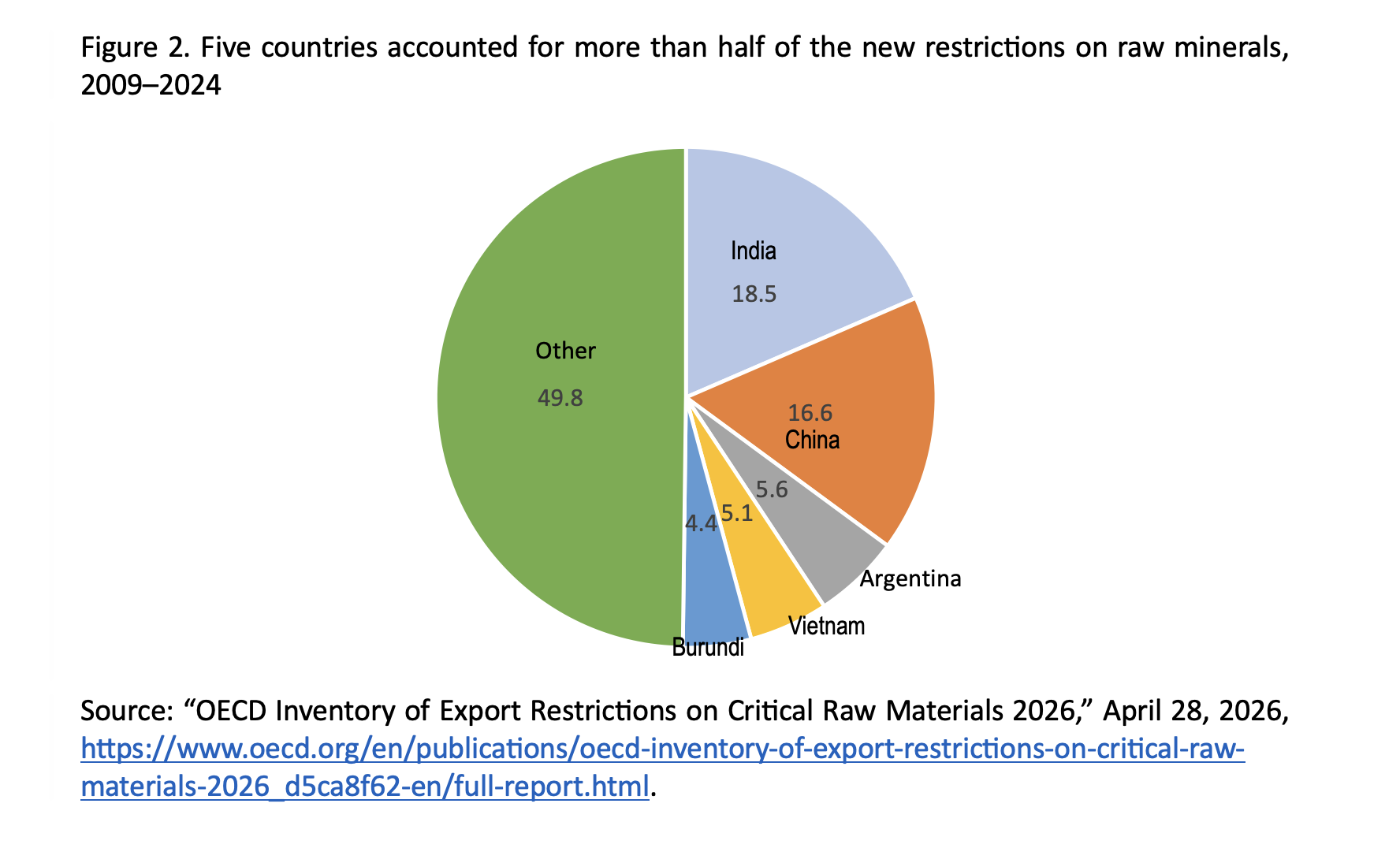

Export taxes and licensing requirements are the most widely used instruments for export restriction. In addition, export prohibitions have become more common. Between 2009 and 2024, the number of countries applying export prohibitions doubled to around thirty. India, China, Argentina, Vietnam, and Burundi introduced the highest numbers of new export restrictions between 2009 and 2024, accounting for slightly more than one-half (Figure 2).

Korea Is One of the Most Exposed Countries

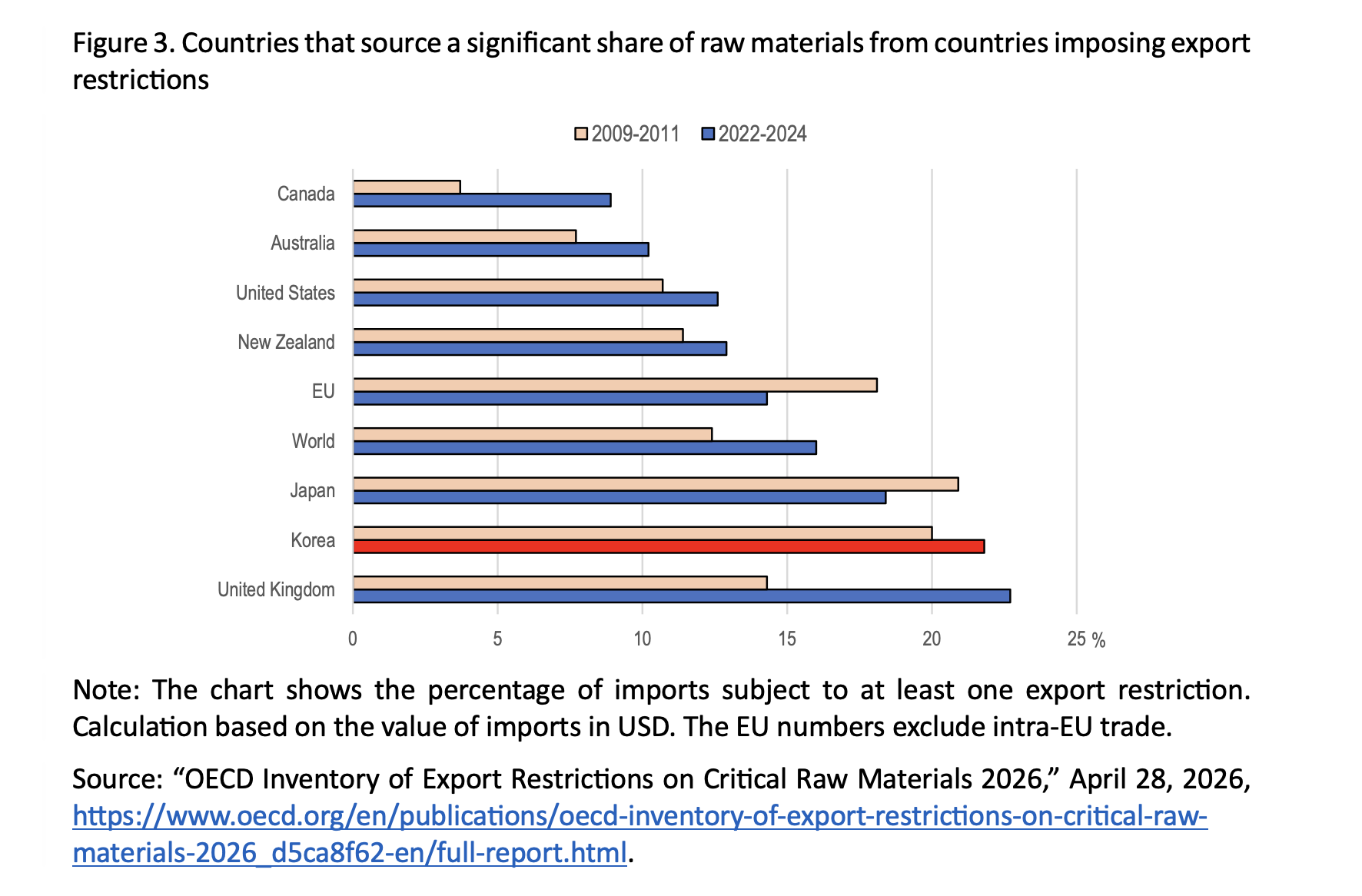

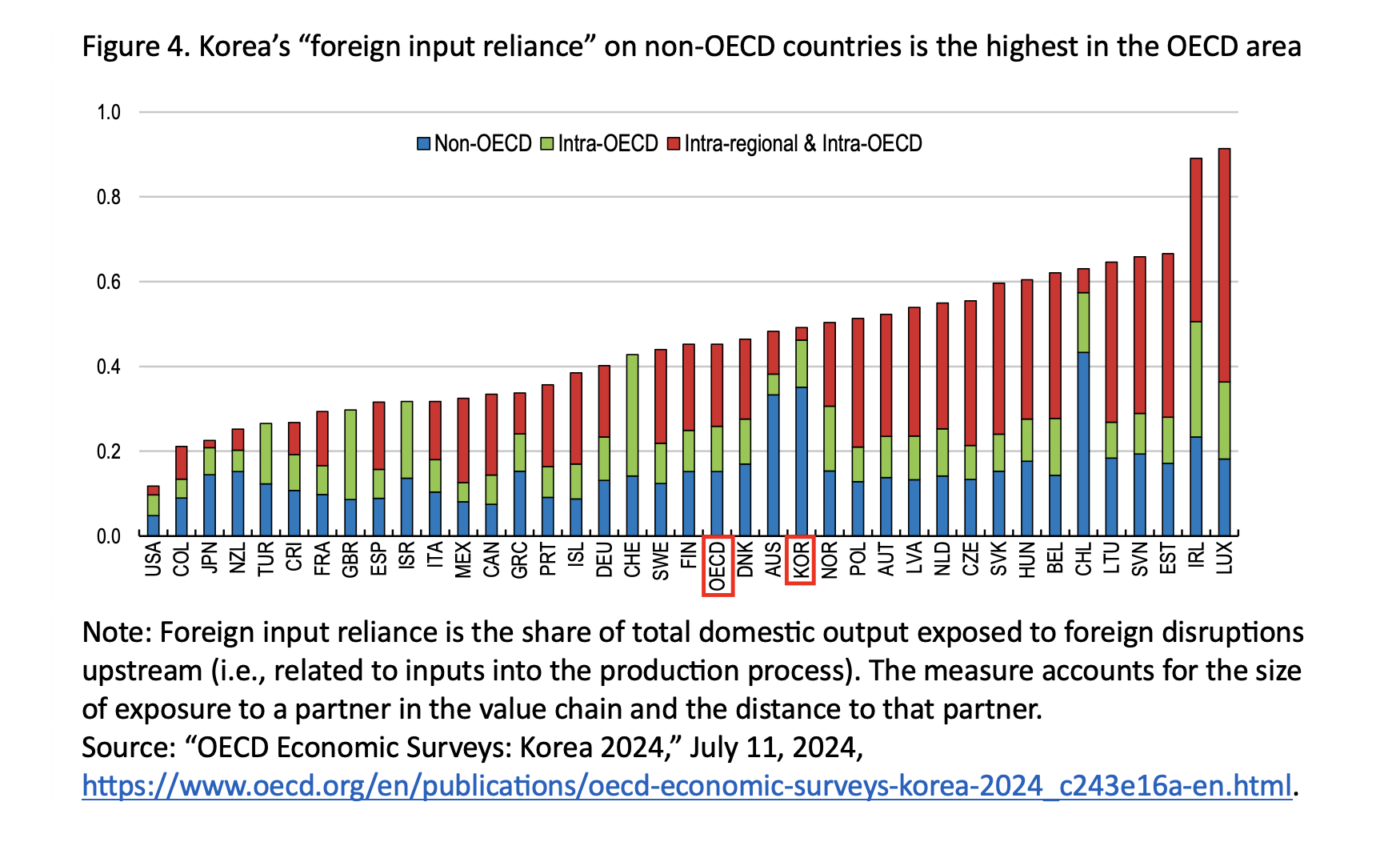

The share of critical raw materials that face at least one export restriction increased globally from 12 percent between 2009 and 2011 to 16 percent between 2022 and 2024 (Figure 3). Korea’s exposure to such restrictions was 21.8 percent over the latter period, well above the global average and the second-highest among OECD countries. In addition, Korea relies heavily on non-OECD countries: it has the highest “foreign input reliance” on non-OECD countries in its upstream value chain—the share of total domestic output exposed to foreign disruptions upstream related to inputs into the production process—among OECD countries (Figure 4).

During the first nine months of 2021, Korea imported 12,586 products (in Korea’s ten-digit Harmonized System), according to the Korea International Trade Association. For almost one-third (3,941) of those products, Korea relied on a single country for 80 percent or more of its total supply. China accounted for 80 percent or more of Korea’s supply in 1,850 materials, including rare earths, followed by the United States (503) and Japan (438).

Dependence on China for manufacturing supply chains creates serious vulnerabilities for Korea’s economic security and global competitiveness. This dependence is especially notable in large-scale and strategic industries, such as chemicals, cars, batteries, and electronics, including semiconductors. One potential bottleneck is magnesium, which Korea imports to manufacture cars, smartphones, and batteries. All of Korea’s magnesium imports come from China, which produces more than 90 percent of the global supply. Moreover, its share of the global production of rare-earth elements is around 70 percent.

Seoul’s Policy Response

It is primarily the responsibility of private companies to reduce their supply-chain dependencies in line with their own business interests. In other words, market forces should help limit supply-chain vulnerability. Companies can accomplish this by expanding domestic production facilities, increasing stockpiles and inventories, and diversifying supply sources (so-called “redundant sourcing”).

However, each of these strategies has a cost and may be rejected by profit-maximizing businesses. While firms tend to manage their own risks without internalizing external effects, the government must consider economy-wide spillover effects. In some cases, the total economic cost of supply-chain dependencies exceeds the private cost to companies, justifying a role for the government. The need for government intervention to ensure supply-chain resilience for national and economic security is greater when supply is concentrated in a small number of countries and firms, or when it is of strategic importance, such as in the case of energy.

The government has launched numerous initiatives to promote supply-chain resilience. In December 2023, it created the Industrial Supply Chain 3050 Strategy, which focuses on 185 “supply chain stabilization items” among imported materials and parts. The Ministry of Trade, Industry and Energy (MOTIE)—now the Ministry of Trade, Industry and Resources—identified these items based on their import dependence and economic importance.

The 3050 Strategy aims to reduce the dependence on these items from specific countries from an average of 70 percent in 2022 to 50 percent or less by 2030 through a range of policies: 1) supporting the development of technology; 2) encouraging mergers and acquisitions; 3) applying regulatory exemptions; 4) recommending that companies expand their inventories and helping them cover the associated costs; and 5) ordering companies to homeshore production in case of an emergency. This was followed in 2024 by MOTIE’s “Eight Major Industry Supply Chain Leading Projects,” which focuses on urea, graphite, battery cathode materials, rare-earth permanent magnets, magnesium, molybdenum, and rare gases used to produce semiconductors.

A second key initiative is the Framework Act on Supporting Supply Chain Stabilization for Economic Security, which took effect in June 2024. The Ministry of Economy and Finance (MOEF) designated 300 “economic security items” eligible for public support to promote stable production and stock management. It also operates an early-warning system for items essential for Korea’s national security. A supply-chain stabilization committee comprising ministers and private experts serves as the control tower for a nationwide supply-chain resilience policy master plan, which will be updated every three years.

In addition, the Export-Import Bank of Korea launched a supply-chain stabilization fund to support private-sector firms in reinforcing their supply chains. The government also plans to gradually expand its stockpiles of twenty key minerals and thirty-five other items to an average of one-hundred days of supply.

Conclusion

The Korean government has taken an active approach to addressing supply-chain risks. At the same time, it is important to limit the economic costs of such policies. Channeling resources to incumbent firms inevitably creates hurdles for emerging firms competing for labor and capital. Likewise, giving resources to incumbent industries can limit opportunities for new emerging industries. Homeshoring of production is likely to enjoy political and popular support but should be a last resort to boost supply-chain resilience because of its high cost. Careful cost-benefit analyses are needed to prevent unnecessary and costly interventions aimed at improving supply-chain resilience.

Randall Jones is a Non-resident Distinguished Fellow at the Korea Economic Institute of America (KEI). The views expressed here are the author’s alone.

This material is distributed by KEI on behalf of the Korea Institute for International Economic Policy. Additional information is available at the Department of Justice, Washington, DC.