Weak U.S. and South Korean GDP Growth in First Quarter of 2025, but for Different Reasons

South Korea will need to improve the performance of its stock markets and small businesses by opening up to foreign portfolio investment

The United States and South Korea scored nearly identical GDP results in the first quarter of 2025 according to newly updated but still preliminary data. Both showed slightly negative change from the fourth quarter of 2024; the United States declining at a negative 0.2 percent rate and South Korea at a negative 0.8 percent rate, both annualized from the fourth quarter. As first quarter data was strongly influenced by unusual U.S. tariff policies and Korean domestic politics, the second quarter should provide a bounce back: a strong one for the United States as imports will slow dramatically, and at least a modest short-term upturn for South Korea provided by the smooth election of Lee Jae-myung and reduced policy rates.

The reasons for the first quarter’s weakness were quite different and are worth considering as we look forward. U.S. weakness is arguably policy-driven—a result of the Trump administration looking to quickly tackle what it sees as long-term unsustainable deficits in both the federal budget and foreign trade accounts, coupled with a commensurate weakness in the traded goods sector driven by disadvantageous trade conditions. This perceived weakness comes alongside a relatively strong dollar as well as foreign tariff and non-tariff barriers that the administration sees as unfair to goods-making workers in the United States. South Korea, especially with its weak currency, is considered an economy of concern in this area. In this way of thinking, the United States has borrowed from the future to give relatively strong GDP results since the COVID-19 crisis, and now the debts are coming due.

South Korea’s weaknesses are more secular—a longer-term slide in its once stellar growth symptomatic of domestic investment faltering amid a host of U.S.- and China-related trade issues along with Seoul’s recent political instability. As inflation has fallen to close to the 2 percent targets in both countries and uncertainty around the effects of U.S. tariffs remains significant, central banks are positioned to address the risk of recession if needed. And, the Bank of Korea acted accordingly last week, lowering its policy rate by a quarter of a percentage point to 2.5 percent.

Longer-term prospects depend on how well the United States can handle its savings shortfalls and dependency on inflows of foreign capital, which includes large amounts from South Korea, China, Japan, and Taiwan. In turn, South Korea’s ability to improve investment conditions at home rests on the ability to raise productivity as its workforce continues its decline due to rapidly aging demographics. The complementarity of the two allies suggests policy cooperation can achieve excellent results, although risks will persist given the U.S. administration’s newfound aversion to imports and South Korea’s historic dependence on exports—and the U.S market—for growth.

U.S. Growth Data Upended by Tariffs

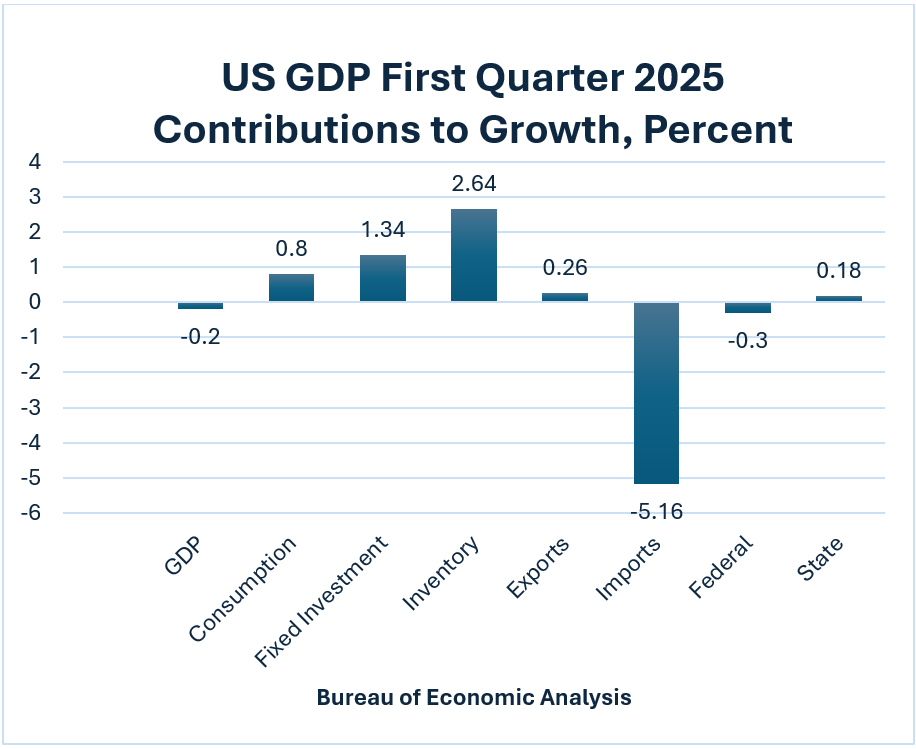

The first quarter data provided by the Bureau of Economic Analysis (BEA) offers a textbook lesson in GDP accounting, one that has confused many media analysts projecting a recession. For the U.S. economy, consumption and fixed investment usually drive growth and both were at relatively strong levels in the first quarter, combined to equal 2.14 percent growth—on trend with the last several years and slightly above predictions for full year GDP growth. But due to the sudden threatened imposition of tariffs, imports shot up in March to get ahead of the tariff curve subtracting a huge 5 percentage points off GDP, annualized.

Unlike GDP, imports are not a component of domestic production. But due to the way the numbers are calculated, imports are reflected in other components of GDP such as consumer and investment goods as well as inventory investment. Imports must therefore be subtracted to avoid double counting, leading to a widespread notion that imports subtract from growth. Imports not immediately consumed go into inventory investment, which adds to calculated growth. These figures jumped along with imports in the first quarter GDP, but likely not by the full amount of the imports increase due to data lags. This phenomenon will all reverse in the second quarter and calculated GDP will rise sharply. In fact, early estimates show GDP may jump at close to a 3.8 percent annual rate in the second quarter as of June 9.

Federal spending also declined in the first quarter and contributed 0.3 percentage points to the GDP decline, as the Trump administration’s agency cuts began to be felt. More of this decline can be expected.

Media—and some forecasters—have reported on the negative aggregate first quarter figure and suggested a recession is at hand, but this outcome seems highly unlikely for now. The IMF growth forecast for the United States for the year was revised down by 0.9 percent but remains positive at 1.8 percent, while a recent OECD forecast puts full-year growth at 1.5 percent.

It is too early to portend smooth sailing for the U.S. economy. Since April, the Trump administration has used 10 percent universal tariffs to fight what it considers unsustainable twin deficits. In January the rolling twelve-month federal budget deficit reached USD 2.1 trillion, or an estimated 7.6 percent of GDP—far above that of most OECD countries. The 2024 current account deficit rose to a record USD 1.13 trillion, or 3.9 percent of GDP, which is also well ahead of the OECD average.

South Korea’s current account, in contrast, was in surplus by 5.3 percent of GDP. U.S. costs of servicing these deficits, as well as resulting debts, are increasing due to both additional debt and to relatively high treasury yields quickly eating away fiscal space. Moody’s lowering of the federal government’s credit rating, catching up with cuts by other credit agencies in the past two years, only reinforces those dangers. Even with Trump’s federal spending cuts, budget issues are not going away. In fact, the issues could become worse as the cost of servicing the debt rises.

Despite the dollar’s current strength and the resiliency of confidence in U.S. treasury securities, there remains the concern that outside investors—especially Chinese, Japanese, Taiwanese, South Korean, and other investors—may at some point decide to pull back on treasury securities purchases that make these deficits possible. The effectiveness of tariffs and federal spending cutbacks in lowering the twin deficits remains to be seen. In a forecast published this week, the Congressional Budget Office (CBO) predicts that the tariff changes to date will lower the federal deficit by a cumulative USD 2.8 trillion over ten years, but also will reduce GDP growth by 0.06 percent per year for a total loss of 0.6 percent by 2035.

While such estimates enjoy bipartisan consensus, they depend on many future policy changes, such as the new budget being proposed by the administration and thus should be considered speculative at best. For instance, there is still uncertainty on whether the tariffs increase the rate of inflation, as the CBO also suggests. Federal Reserve Chairman Powell predicts a nasty combination of higher inflation and slower growth due to the tariffs. As he noted, inflation expectations can be self-fulfilling, but tariffs, in theory, should raise federal income and thus lower the need for inflation-inducing monetary expansion while reducing demand and thus growth. Recent data moreover shows a continuing decline in the rate of price increases. The Consumer Price Index will likely show a one-time jump in imported goods prices in the coming months, but how persistent such increases will be is a matter of much conjecture.

South Korea confronts declining investment, weak won, and export disruption

South Korea’s slowdown is more structural than it is policy-driven, exacerbated by the recently unsettled domestic political situation as well as by U.S. tariffs, both of which depress domestic investment spending. The new Lee government and the central bank are both in a difficult position as they must react to conditions outside their control that could push growth below zero or raise inflation. Further policy rate declines, for instance, could further drop the won. This lack of leverage is ironic since the country has a huge net positive foreign investment position, a large current account surplus, and a fiscal deficit and public debt that are much smaller relative to GDP than they are for the United States or other OECD countries. One might think these assets would give the government greater leverage to drive policy. Yet the won is weak as foreign investors hesitate to buy in, and South Korean savers easily invest out, making it difficult for the Bank of Korea to lower interest rates to encourage domestic investment.

The first quarter data shows a key problem is declining domestic investment, especially in the interest-sensitive construction sector. Following a post-COVID-19 recovery, slowing private domestic investment has pulled down aggregate GDP growth every quarter, falling to a minus 0.7 percent in the first quarter.

Much like in China, overbuilding in the past has led to huge contractions in current construction, resulting in a downturn. Facilities investment, especially in the semiconductor industry, had been strong but also fell sharply in the first quarter, probably because of the U.S. tariffs and political unrest.

Weak export prospects further weigh on the economy, although in theory the weak won (not just relative to the strong dollar but also to other currencies) should help with exports. But with a weakening won over time, Korean private investment is flowing overseas, further depressing the currency in a negative spiral. Higher interest rates at home needed to counteract the won’s decline would further exacerbate domestic investment issues; hence the Bank of Korea’s dilemma in adjusting rates, which finally decided on the 0.25 percentage point cut just before the election.

Nonetheless, South Korea’s large positive net foreign assets and the government’s long history of conservative spending remain an advantage to the economy. Indeed, Seoul habitually runs much lower fiscal deficits than do its OECD peers despite its large defense spending requirements. The late interim government sought to boost government spending to boost GDP growth. President Lee will likely do the same, but he will have to be cautious given the long-term budget worries of a rapidly aging population.

Policy Decisions Will Drive 2025 Growth in Both Countries

U.S. tariffs, budgets, and monetary policies all aimed at unsustainable deficits will keep short-term growth modest; below 2 percent in 2025 according to most forecasters, after a big jump in the second quarter that will offset the first quarter slump. The Trump administration has said that there may be economic pain before its pro-growth policies take real effect. As baseball pundits might say, “it is a rebuilding year.” But these efforts will impact South Korea as it is highly linked to the U.S. economy. Revised economic forecasts for South Korea are even a bit slower than for the United States, at less than 1 percent. With negative population growth, the per-capita estimates of the two countries are about the same. Seoul will likely boost public spending as Washington seeks to do the opposite to try to reduce its twin deficits.

There is irony in how similar the outcomes are given the two countries’ far different savings and investment habits: the United States with weak savings and strong investment, and South Korea with strong savings and weak investment. South Koreans have long been wary of bringing in too much investment from its big economic partners—the United States, China, and Japan—for fear of its firms losing their independence. South Korea will need to improve the performance of its stock and bond markets, and ultimately the profit performance of small and medium-sized firms, by making South Korea more conducive to foreign portfolio investment (e.g., non-controlling investment by foreign individuals). These measures could flip the won and the investment shortfall simultaneously to give the economy needed positive momentum. Both countries could benefit from such a rebalancing.

This is an opinion piece by William Brown, Distinguished KEI Fellow. Brown is retired from Federal Government service including ten years in the Commerce Department’s Office of the Chief Economist, the unit that overseas release of U.S. national account data. He also has worked extensively on East Asian economies in the U.S. intelligence services.

Photo from Shutterstock.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.