Search All Site Content

Total Index: 6913 publications.

Subscribe to our Mailing List!

Sign up for our mailing list to keep up to date on all the latest developments.

The Peninsula

The Rise of K-Beauty and the Economic Implications for South Korea

South Korea’s cosmetics industry has become one of the country’s most dynamic export engines, transforming from a cultural curiosity into a high-value sector that demonstrates how innovation, soft power, and macroeconomic conditions can converge to reshape a nation’s trade profile. What began as a wave of interest in Korean skincare routines has matured into a global industry with a measurable impact on Korea’s export diversification strategy, particularly as traditional manufacturing sectors face slowing demand and rising competition.

The conventional narrative credits the U.S.-South Korea Free Trade Agreement (KORUS FTA) for opening doors to the U.S. market. While tariff liberalization played a foundational role, the trajectory of K-beauty over the past decade suggests a more complicated story. Exchange-rate competitiveness, digital-first distribution models, and the global elasticity of demand for premium skincare products now rival—and in some cases outweigh—the benefits of tariff reduction.

Seen through this lens, K-beauty’s rapid ascent is more than an export success story. It is a case study of how advanced economies compete across industries through branding, innovation, and agility to respond to macroeconomic volatility.

Global Trajectory and U.S. Expansion

Korea’s cosmetics industry has moved beyond trend-driven consumption and matured into a key export pillar. Between 2020 and 2024, Korea’s total cosmetics exports expanded from USD 7.57 billion to USD 10.23 billion, representing a cumulative increase of 35 percent. This growth occurred against the backdrop of a global pandemic, volatile energy markets, and shifting trade regulations, underscoring the adaptability and consumer pull of Korean beauty products.

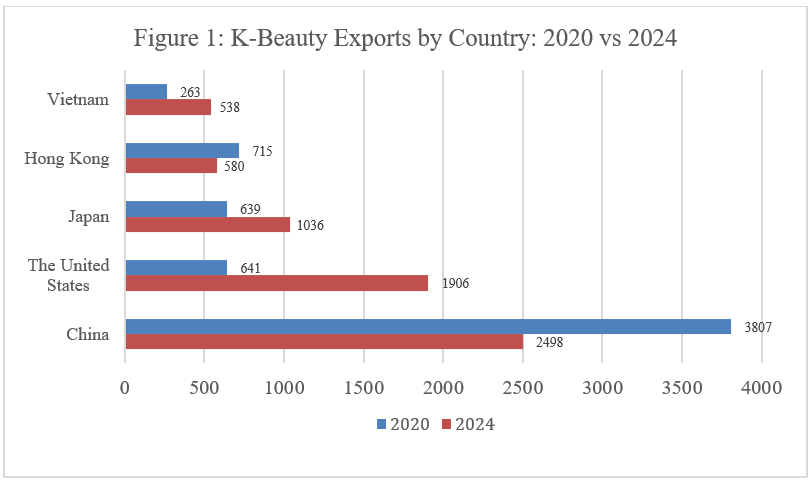

Figure 1. K-Beauty Exports by Country, 2020 vs. 2024

Source: Korean Ministry of Trade, Industry and Energy

As illustrated in Figure 1, the composition of Korea’s export destinations has shifted in the first half of this decade. While China remained the largest recipient of Korean cosmetics in both 2020 and 2024, exports to China declined by over USD 1.3 billion, falling from USD 3.81 billion to USD 2.50 billion. In contrast, exports to the United States rose sharply, from USD 641 million to USD 1.91 billion, effectively tripling in just four years.

This striking reversal reflects deeper dynamics in global demand: where China once served as the single-largest growth engine for K-beauty, North America has now emerged as a principal frontier market, particularly in skincare.

Korean beauty firms have leveraged the regulatory certainty and zero-tariff environment provided by the KORUS FTA, as well as the scalable nature of the U.S. e-commerce ecosystem. In doing so, they have broadened their reach among North American consumers, particularly millennials and Generation Z, who increasingly seek dermatologically advanced, cruelty-free, and culturally distinctive skincare brands. Industry analysts and market observers frequently describe Korean beauty products as emphasizing innovation, novel formulations, and science-oriented skincare development, contributing to a global reputation for technologically sophisticated beauty products. In contrast, China’s decline is multicausal. Rising protectionism, more competitive domestic brands, tightened cross-border trade controls, and the resurgence of nationalistic consumer behavior have contributed to a cooling of demand for foreign beauty goods, including those from Korea. Yet, rather than contracting, Korea’s total export value continued to rise—driven by diversification across Vietnam, Japan, and especially the United States.

The trajectory of Korean cosmetics exports is increasingly defined by global market differentiation. Its expansion into the U.S. market, in particular, suggests that Korea’s cosmetics sector may be approaching a new phase—one in which its resilience is measured not by volume alone, but by its ability to generate value-added exports across geographies. In that respect, U.S. consumer demand for K-beauty imports may serve as a bellwether for Korea’s broader ambitions in post-industrial export growth.

Competitive Leverage in the U.S. Cosmetics Trade

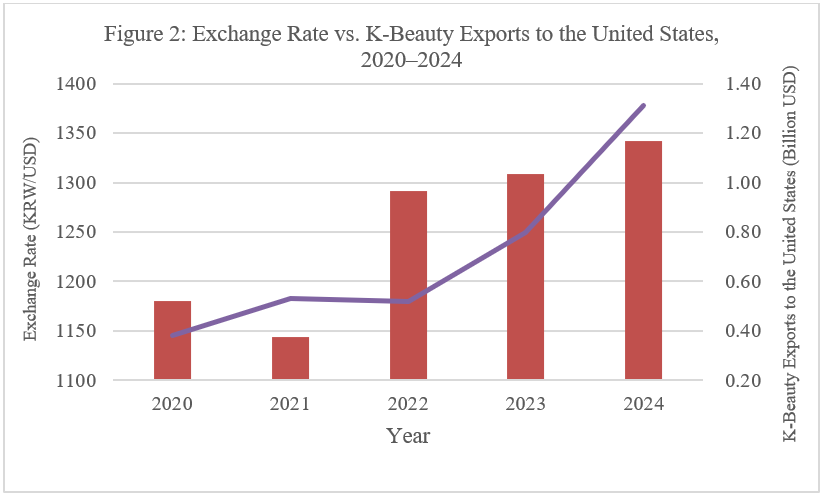

The competitiveness of Korea’s cosmetics exports is shaped not only by consumer trends and cultural influence, but also by macroeconomic fundamentals—most notably, exchange rates. While tariff structures implemented under the KORUS FTA have helped stabilize Korea’s access to U.S. markets, currency fluctuations have emerged as a more influential determinant of export volume growth in recent years. As illustrated in Figure 2, there is a positive correlation between the depreciation of the Korean won against the U.S. dollar and the rise in K-beauty exports to the United States.

Figure 2. Exchange Rate vs. K-Beauty Exports to the United States, 2020–2024

Source: UN Comtrade; Bank of Korea

Between 2020 and 2024, the exchange rate of the Korean won against the U.S. dollar increased from 1,180 to 1,342, reflecting sustained depreciation of the won. Over the same period, Korean cosmetics exports to the United States expanded from USD 381 million to over USD 1.3 billion, a more than threefold increase. While this growth is partly attributable to rising consumer demand and brand recognition, the timeline closely aligns with the weakening of the Korean won—effectively making Korean products more price-competitive in dollar-denominated markets.

Equally important to the sector’s structural advantage is the complete removal of U.S. tariffs on Korean skincare products under the KORUS FTA. Prior to the agreement’s implementation in 2012, the Most Favored Nation (MFN) tariff rate for beauty products was 5 percent. These rates were gradually reduced, dropping to 3.3 percent in 2012, 1.7 percent in 2013, and ultimately reaching zero by 2016. The resulting regulatory certainty allowed Korean firms to enter the U.S. market without tariff-related cost disadvantages, especially compared to non-FTA competitors. As a long-term policy instrument, the KORUS FTA provided a stable institutional framework that reduced trade-related cost uncertainty. Literature on trade liberalization suggests that such exposure to international competition encourages exporting firms to engage in product quality upgrading and strategic differentiation, creating conditions under which Korean exporters could reallocate resources to focus on higher-value activities such as branding, formulation development, and global marketing.

Exchange rate effects are particularly relevant for small and medium-sized cosmetics exporters, whose cost structures are more sensitive to currency shifts. A weaker won improves their price flexibility in global markets without requiring cuts to product margins. This has allowed Korean firms to compete more effectively in the United States against both premium European labels and emerging domestic beauty brands. Importantly, the price advantage created by currency shifts complements, rather than substitutes for, tariff-free access under the KORUS FTA, which has maintained a zero-tariff rate on skincare and cosmetic goods since 2016.

From a policy standpoint, Korea’s experience in the cosmetics sector underscores that in export industries where tariffs are already low, exchange rate competitiveness becomes a primary lever of trade performance. This suggests that macroeconomic coordination—particularly regarding exchange rate stability and hedging instruments—should be viewed as part of Korea’s non-manufacturing export strategy.

Elastic Demand and the Strategic Leverage

In assessing the resilience and responsiveness of Korea’s cosmetics industry to global economic shocks, one key metric is the price elasticity of exports—a measure of how export volumes respond to changes in relative prices, including currency-driven price shifts. Korea’s cosmetics sector displays remarkably high price elasticity compared to other consumer goods.

According to World Bank research, the average export elasticity for advanced economies is approximately 1.4, while developing economies are closer to 0.6. Given South Korea’s status as a high-income country with a mature, innovation-driven cosmetics industry, it is reasonable to expect relatively high elasticity. But recent trends in Korean cosmetics exports—particularly to the United States—suggest that elasticity in this sector may be significantly higher.

A simple log-difference elasticity estimate using 2020–2024 data indicates that a 1 percent depreciation of the Korean won was associated with a 6–12 percent increase in exports to the United States, pointing to an exchange-rate elasticity far above benchmark levels. Part of the explanation for this is the “premium” image many K-beauty manufacturers have cultivated, coupled with relatively low unit production costs, which enable firms to scale up quickly as price competitiveness improves.

According to OECD trade data, industries that rely heavily on expensive equipment, such as cars or home appliances, tend to adjust their export levels slowly because production is capital-intensive and supply chains move at a slower pace. Cosmetics behave very differently. Even compared to other fast-moving consumer goods, Korean beauty products show unusually quick shifts in export volume when prices change. This is partly because K-beauty brands operate in an e-commerce ecosystem where new prices, promotions, and product launches reach consumers almost instantly, allowing demand to grow faster than in other sectors.

From a policy perspective, this high elasticity offers both opportunity and risk. It allows K-beauty to serve as a shock-absorbing export sector, helping offset volatility in Korea’s manufacturing-heavy trade portfolio. But it also implies a higher degree of exposure to currency and price swings, especially in high-demand markets such as the United States, Japan, and Southeast Asia. Export promotion strategies, therefore, should not only focus on branding and innovation but also on hedging tools, foreign exchange stabilization, and real-time price monitoring infrastructure for small and medium exporters.

Conclusion

Cosmetics are increasingly central to Korea’s non-manufacturing export strategy. While the KORUS FTA created the regulatory and tariff environment that allowed Korean beauty firms to scale rapidly in the United States, Washington’s recent cleave toward trade barriers and protectionism has introduced new complexity.

The core question is whether K-beauty’s export boom can persist even in the partial absence of stable tariff advantages. The evidence suggests yes, though with caveats. Recent growth reflects a confluence of high exchange-rate elasticity, consumer-driven product differentiation, and the structural adaptability of Korean firms in online markets.

The next phase of Korean economic strategy in this space must focus not only on negotiating access but on sustaining advantage amid unpredictable trade rules and geopolitical uncertainty. K-beauty’s success thus serves as a case study of how branding, innovation, and macroeconomic alignment can generate export value in a post-tariff, post-industrial global economy.

Soeun Jeon is a researcher at the National Women in Agriculture Association (NWIAA). All views presented here are the author’s alone.

Feature image from Shutterstock.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.