By Tom Ramage

The Iran War Is Stress-Testing South Korea’s Energy Model

Rapid fuel price jumps, supply shortages, and tightening windows for reserves will likely prompt a reevaluation of international energy trade.

Listen to this article

0:00 / 0:00

The global price of oil hit USD 119 a barrel last week, and few countries are as vulnerable to the sudden increase as South Korea. Korea imports nearly all its energy and ships most of its crude oil through the Strait of Hormuz, which is now effectively closed. The country has imposed gas price caps, begun tapping strategic reserves, and faces mounting strategic material shortages that threaten semiconductor output.

The crisis is accelerating a rethink of how Korea powers itself. Emergency measures such as lifting limits on coal-fired generation and expanding nuclear energy utilization are buying time, but long-term measures, like securing access to U.S. energy resources that would route fuel through the Pacific Ocean rather than through Middle Eastern chokepoints and efforts to expand alternative energy capacity, may place Seoul in a new position following the crisis altogether.

Strait of Hormuz and Korea’s Oil Imports

Iran is attacking commercial and naval vessels that try to pass through the Strait of Hormuz as part of a broader retaliation against the United States and Israel. This has resulted in an effective closure of the Strait, through which 20 percent of the world’s oil and liquified natural gas passes.

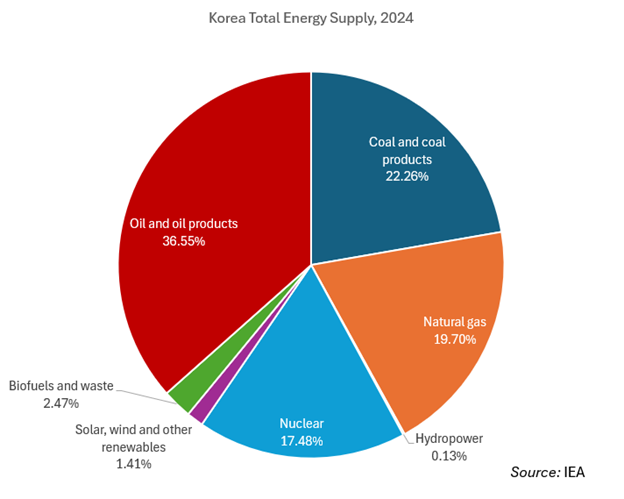

The effects have been deleterious for Korea, which imports close to 94 percent of its energy resources from abroad, including 70 percent of its crude oil via ships transiting through the Strait. To some extent, the fallout has been tempered by the country’s efforts to diversify its energy portfolio and emergency measures to tap strategic oil reserves. But rapid increases in fuel prices, supply shortages of petroleum-derived strategic materials, and tightening windows for reserves of products such as liquefied natural gas (LNG) are likely to prompt Korea to reevaluate its overall position in international energy trade.

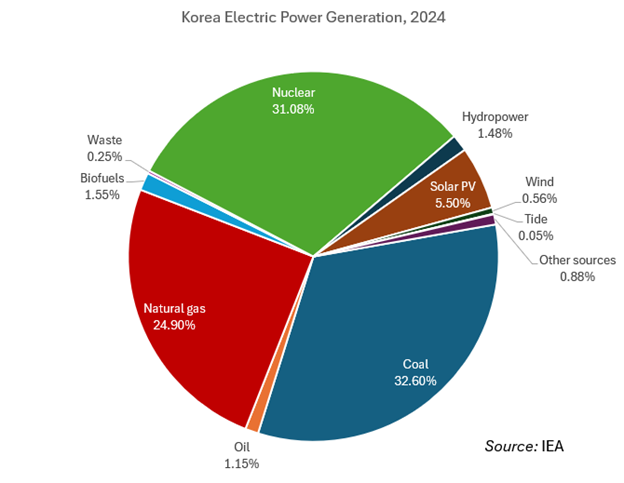

Coal and natural gas make up the majority of Korea’s energy portfolio. The Iran crisis has an immediate impact on Korea’s access to the LNG it uses for more than 19 percent of its total energy supply and roughly 25 percent of its electric power generation. As of 2025, some 15 percent of Korea’s LNG imports came from Qatar, located behind the blocked Strait of Hormuz. This is behind Malaysia (16.1 percent) and ahead of the United States (9.4 percent). Following an Iranian attack on Qatar’s Ras Laffan gas facility, Qatar’s national gas company declared force majeure on some of its long-term gas contracts, excusing them from obligations to fulfill them.

Korea’s Ministry of Trade, Industry and Resources has indicated that the country’s LNG reserves are sufficient “for a considerable period, even if imports from Qatar are completely halted.” Indeed, the effects on Korea are perhaps more blunted than they would have been in prior years, when Korea had more LNG imports from Qatar; Korea’s LNG imports from the country decreased by 6.9 percent from 2022 to 2025, and regional partners like Australia are playing a larger role. But LNG supplies could be disrupted for an extended timeframe due to the strikes on Qatari gas fields, meaning higher prices could stick around well beyond the cushion of Korea’s LNG reserve stockpiles.

Immediate Impacts on the Korean Economy

The Iran war may incentivize Korea to diversify its energy sources away from the Middle East. More immediately, disruptions in the gas trade as a result of the crisis will likely increase domestic reliance on Korea’s coal sector, which comprises roughly 33 percent of the country’s electric power generation, and hasten the speed at which nuclear power generation comes online. The Korean government has since stated that Korea will lift limits on coal power generation and increase nuclear plant utilization to up to 80 percent.

As for oil, this has broader economic effects on inflation and household spending, prompting government efforts to encourage price stability. Rising oil prices in Korea have prompted the imposition of price caps on gas for the first time in thirty years. Seoul has joined other International Energy Agency (IEA) member countries in initiating a targeted release of its strategic oil reserves to stabilize prices. This may buy some time to avert a widespread economic crisis because of high fuel prices. Still, the associated effects may slightly reduce Korea’s overall growth this year from 2 percent to 1.9 percent.

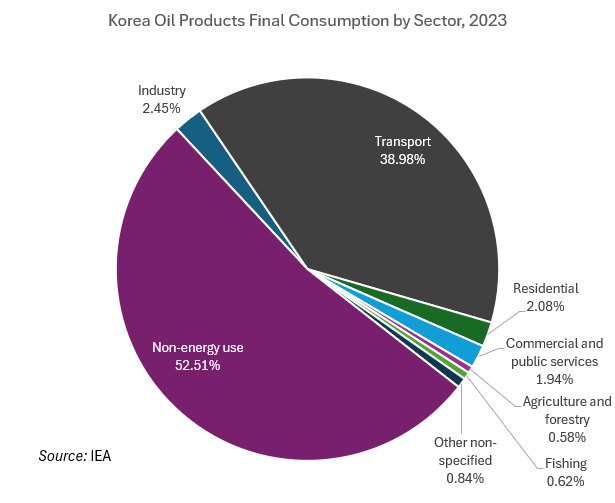

For example, the effects of the oil shocks are hard felt in the industrial sector. While oil accounts for a majority of Korea’s total energy imports, it is primarily used for “non-energy use” (including the manufacturing of advanced products such as semiconductors), followed secondarily as fuel for transportation. The combination of high-energy costs and volatility in industrial inputs for advanced technology products has the potential to cause a ripple effect in the Korean and global economies for as long as the conflict continues. Shortages in naphtha—a chemical additive critical for the production of synthetic fibers used downstream in industries such as semiconductor and automobile production—have further prompted the Korean government to place it on a list of “economic security” items and establish a support fund for companies impacted by the supply chain disruptions.

Gas field closures have also obstructed Korea’s access to helium, a critical component for semiconductor manufacturing. Roughly 65 percent of its supply comes from Qatar. Chemical fertilizer—another byproduct of LNG production—also faces supply shocks from a prolonged conflict in Iran.

While accounting for shortages in strategic materials can only be addressed by diversifying Korea’s import sources for petroleum products, one way of mitigating the energy aspect of future resource shocks will likely involve increasing the share of alternative energy sources in Korea’s portfolio. Korea has been proactive in promoting renewable energy capacity to meet its electric power generation needs, with solar, wind, and biomass accounting for an increasing share of the country’s domestic energy consumption.

Nuclear energy is also already well on its way to powering a larger share of Korea’s energy needs, driven by AI. It is possible that momentum in the nuclear energy sector will prompt discussions between the United States and Korea on autonomous nuclear fuel reprocessing and other cooperative measures. Doing so would take advantage of Korea’s largest domestic energy source. Of the roughly 607 TWh generated for electricity consumption in 2024, more than 31 percent came from nuclear—the second-largest source of electric power generation behind coal.

U.S. Energy Appeal

Beyond the initial shocks of the crisis, the Iran war will also likely drive larger energy purchases from the United States and other partner countries. Korea was the fourth-largest importer of U.S. oil in 2025 and remains a major destination for U.S. LNG shipments. Similar to Japanese investments under the U.S.-Japan memorandum of understanding (MOU), investment participation in U.S. LNG and oil facilities is rumored to comprise a large portion of Korean investment commitments in the United States, while the U.S.-Korea trade deal commits USD 100 billion toward the purchase of U.S. energy products.

Although the U.S. Department of Energy projects LNG imports will play a smaller role in Korea’s energy generation going forward, its use as a transitional fuel and increasing flexibility in sourcing could allow it to serve as an interim anchor of Korea’s electric power generation as the country approaches its net-zero 2050 initiative. Against this backdrop, investments in foreign energy projects, particularly in the United States, could serve as a bulwark against chokepoints and volatility in future energy crises.

For example, the development of export terminals and pipeline infrastructure could allow LNG and oil to transit to Korea across the Pacific rather than through the Middle East, acting as a hedge against long-term geopolitical supply chain disruptions. Such investments would also expand opportunities for Korean-built LNG carriers to play a larger role in the U.S. energy trade. It will be up to the U.S.-Korea investment committee, however, to determine if such projects make economic and strategic sense under the terms of the MOU.

In any case, increases in energy prices and shortages in supplies of key materials are bound to take months to years to recover. The effects beyond energy will be manifold: economic reverberations from the spikes in oil prices and supply chain shortages, short-term pressure on the Korean won and KOSPI index, billions of dollars in Korean investment projects across the Middle East at risk of being delayed, and undue pressure placed on the U.S.-Korea alliance. It is unlikely that the global environment will easily snap back to the way it was before.

Taking everything into account, the Iran conflict may not only redefine Korea’s domestic energy priorities but also its overall place in the international energy, economic, and security system. Its effects will initiate lasting changes to how energy is sourced, used, and prioritized.

Tom Ramage is Economic Policy Analyst at the Korea Economic Institute of America (KEI). The views expressed are the authors’ alone.

Feature image from Shutterstock.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.