Inflation and the Ukraine War Still Holding Back Korea’s Economic Outlook

Korea's new economic outlook is a slight downward revision from the OECD’s November 2022 outlook in the context of global economic growth.

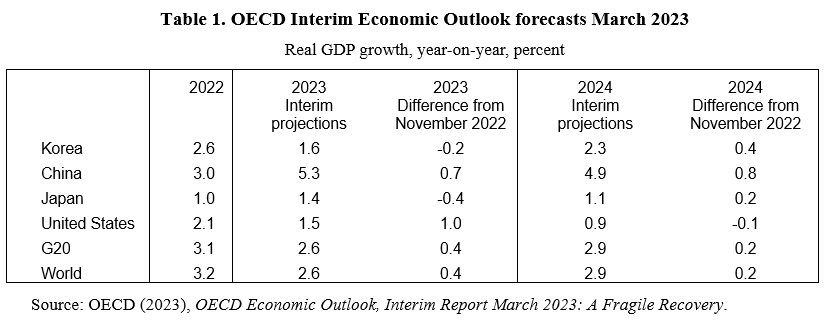

The OECD’s March Interim Economic Outlook projects that Korea’s real GDP will increase by 1.6% in 2023, matching the Bank of Korea’s February forecast. The new projection is a slight downward revision from the OECD’s November 2022 outlook in the context of below-trend global economic growth. The impact of the war in Ukraine and high inflation has held back the global economy. Some positive signs, such as the decline in food and energy prices and the full reopening of China, should lead to faster growth in 2024 in Korea and the world economy. However, there are many downside risks, notably the consequences of Russia’s invasion of Ukraine. In addition, the impact of monetary policy tightening is difficult to judge and could lead to further financial vulnerabilities in many countries.

Weakness in Korean exports and domestic demand

Since the final quarter of 2022, the downturn in the tech sector has been a drag on the Korean output and exports. In the March Green Book assessment of the economy, the Ministry of Economy and Finance stated, “With exports remaining sluggish and manufacturers’ business sentiment contracting, the trend of an economic slowdown has continued.” According to the Korea Development Institute’s monthly economic report, “The manufacturing sector is undergoing a considerable contraction, marked by a sharp decline in production and an evident increase in inventories, especially semiconductors”. Indeed, exports of semiconductors, Korea’s major export, fell 42.5% in February 2023 from a year earlier in U.S. dollar value. The manufacturing downturn has resulted in a fall in business-sector investment in equipment and slower employment growth.

In addition, domestic demand has been negatively affected by higher interest rates. Private consumption is gradually slowing as retail sales stagnate and service production growth decelerates. Indeed, retail sales fell 2.1% (month-on-month) in January. A weaker real estate market in the context of high interest rates has hit construction investment.

Brighter prospects for exports in 2023

Although real indicators remain disappointing, Korea’s economic sentiment index is improving in anticipation of a recovery, mainly driven by the reopening of China, which accounts for about a quarter of Korean exports. The Ministry of Economy and Finance stated, “We expect the normalization of industrial activities in China will have significant positive impacts on exports in our manufacturing sector.” In addition, a resumption of overseas travel by the Chinese would benefit Korea. Before the pandemic, Chinese tourists accounted for one-third of Korea’s foreign visitors.

Although Japan is a less important trade partner (less than 5% of Korean exports), increased trade with Japan could be another positive factor following the summit between President Yoon Suk Yeol and Japanese Prime Minister Kishida Fumio in Tokyo in mid-March. In 2019, Japan imposed export controls on three materials (fluorine polyimide, photoresist and hydrogen fluoride) that are critical for producing semiconductors and flexible displays. In addition, it removed Korea from its “whitelist” of trusted trade partners. After Korea announced earlier this month that it would compensate victims of Japan’s wartime forced labor without asking Japan for contributions, Tokyo decided to remove its export controls.

Korea’s Minister of Economy and Finance, Choo Kyung-ho, said this move would “give a significant positive spillover to our economy.” He added that, “considering the normalization of the supply chain of key products, including semiconductors, along with the bilateral cooperation in cutting-edge sectors, the economic effect (of restoration) will be even bigger”. The Korea Chamber of Commerce and Industry projected that Korea’s exports to Japan would rise by KRW 3.5 trillion ($2.69 billion). It also predicted that the steel, petrochemicals, electronics and auto parts industries would be the primary beneficiaries. However, President Yoon’s proposed solution is politically unpopular, with a Gallup Korea poll reporting that 59% of Koreans are opposed.

Monetary policy and inflation

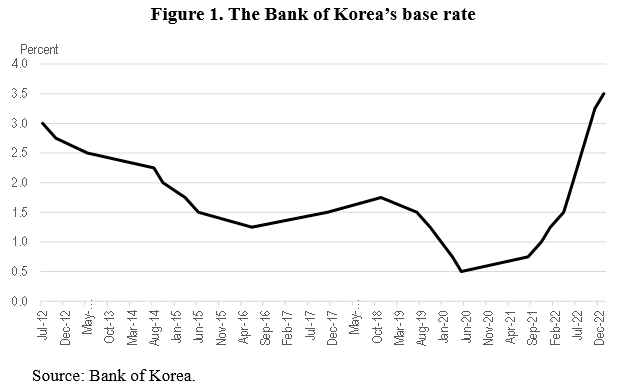

Korea’s economic outlook will also depend on monetary policy and progress in reducing inflation. Consumer price inflation peaked at 6.3% in July 2022, its highest rate since 1998, driven by soaring energy costs. The Bank of Korea responded with a series of hikes in its policy rate (the base rate), which had been cut to 0.5% in May 2020 during the COVID-19 pandemic (Figure 1). Since August 2021, ten hikes have lifted the rate to 3.5% in January 2023.

House prices in Korea have fallen nearly 7% (in nominal terms) since May 2022 as interest rates climbed. For the year 2022, apartment prices in Seoul dropped 22%, the largest decline ever. Apartment sales in Seoul, which used to average 6,000 to 8,000 per month, fell to only 559 in October 2022. In January 2023, though, apartment prices in Seoul rose for the first time in seven months as the government removed the capital (except for the Gangnam and Yongsan districts) from the list of “real-estate speculation zones,” which are subject to tighter regulations. However, house prices outside of Seoul continue to decline.

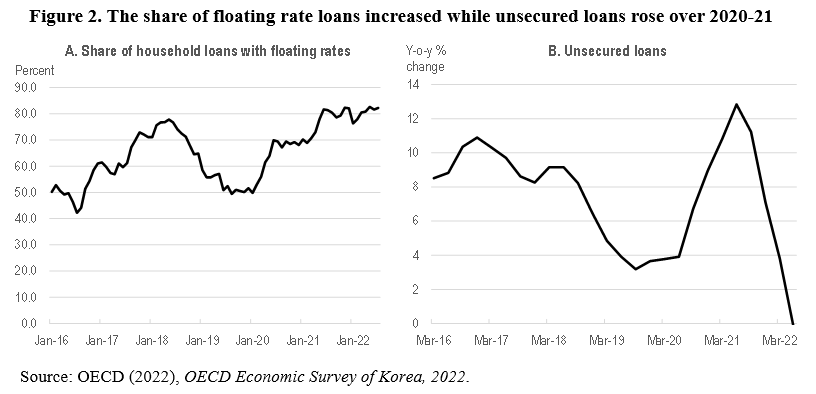

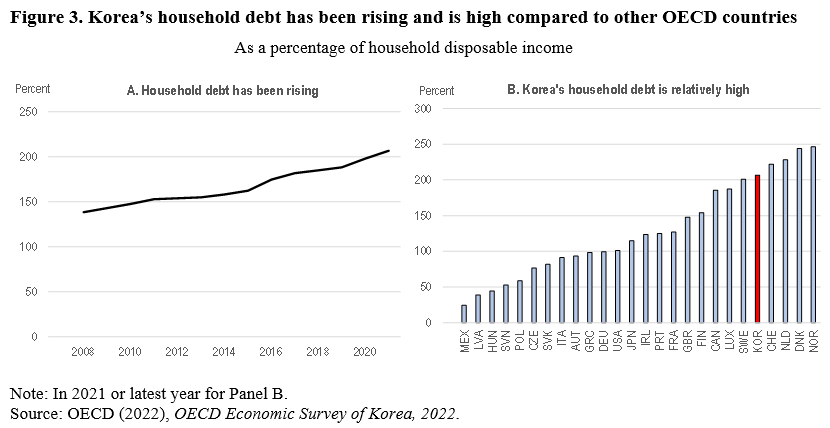

Housing-related loans accounted for about 80% of banks’ total loan portfolio at the end of 2020, increasing their exposure to the real estate sector. More than 80% of total new loans have floating interest rates, implying that households’ debt servicing burden has risen significantly as interest rates increased (Figure 2, Panel A). Unsecured loans, which are largely related to housing, have also grown, especially from non-bank sectors (Figure 2, Panel B). Household debt has risen rapidly over the past decade, surpassing 200% of net disposable income in 2021, one of the highest among OECD countries (Figure 3). Higher interest rates have significantly boosted the debt-service burden on households.

The pace of economic growth will partly depend on monetary policy and its success in reducing inflation. The Bank of Korea left its base rate unchanged in February 2023 for the first time in a year. The pause may have reflected the drop in inflation to 4.8% in February amid signs of economic weakness. In the minutes of the February Monetary Policy Board meeting, one of the members stated, “Given the time lag in monetary policy, we believe it is time to assess the effects of policy spillovers and consider further hikes based on developments of inflation and external and domestic uncertainties” (Yonhap, 2023). However, further hikes are likely with inflation still far above the 2% target. In addition, one member of the Monetary Policy Board noted the wide interest rate gap with the United States. With the Fed’s 25 basis-point hike last week, the gap between U.S. and Korean interest rates has reached 1.5 percentage points, the largest ever, creating concerns about a capital outflow from Korea. Although the interest rate gap is only one of many factors that determine exchange rates, the prospects of additional hikes by the Fed may increase the likelihood that the Bank of Korea will follow suit.

Conclusion

The OECD projects that Korea’s inflation rate will fall to 2.4% in 2004, suggesting that the series of interest rate hikes may be approaching an end, improving the growth outlook. Achieving stronger growth will depend on a correction of the downward cycle in the semiconductor industry and a pick-up in the global economy. However, Russia’s invasion of Ukraine and the financial risks associated with high inflation and rising interest rates in many economies poses risks.

Randall S. Jones is a Non-Resident Distinguished Fellow at the Korea Economic Institute of America. The views expressed here are the author’s alone.

Photo from Shutterstock.