Search All Site Content

Total Index: 6336 publications.

Subscribe to our Mailing List!

Sign up for our mailing list to keep up to date on all the latest developments.

The Peninsula

Beijing’s Economic War on Pyongyang

By William B. Brown

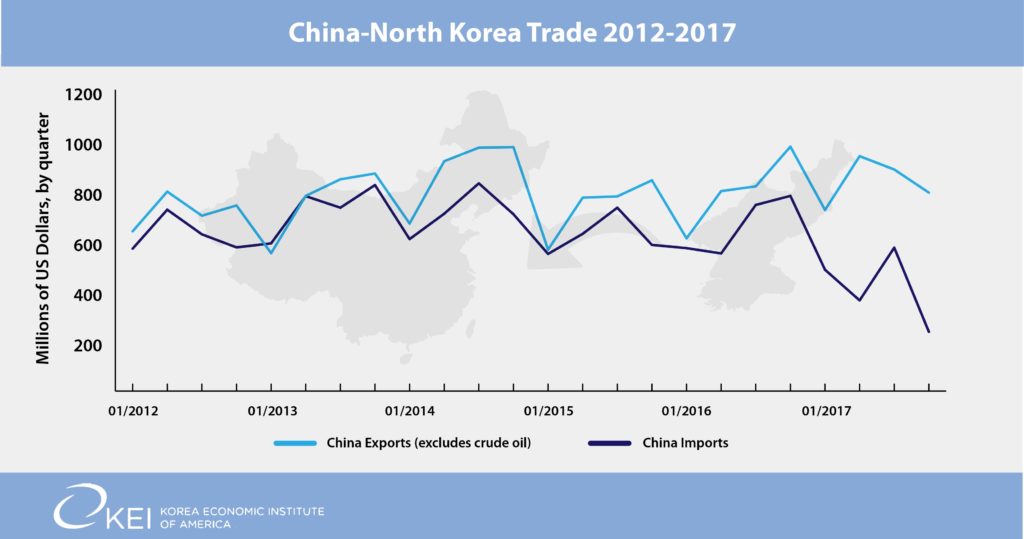

“War” might be a little strong, but I think everyone would agree it’s at least a fierce and growing skirmish. China’s Customs Bureau on Friday reported a sharp, 23 percent drop in exports to North Korea in December from the year-earlier month, to $258 million, and a stunning 83 percent drop in imports, to only $51 million. Quarterly data (graphic below) show the same trend, with exports down 20 percent and imports down 70 percent. For all of 2017, Chinese exports inched up 4 percent to $3.33 billion while imports fell 37 percent to $1.65 billion, driving its surplus, North Korea’s deficit, to record levels. To put the data in perspective, North Korea ranked 87th among China’s suppliers in December, somewhere between Solomon Islands and Armenia; South Korea ($17.2 billion.) ranked first, every day selling what North Korea sells in a year at recent rates.[i]

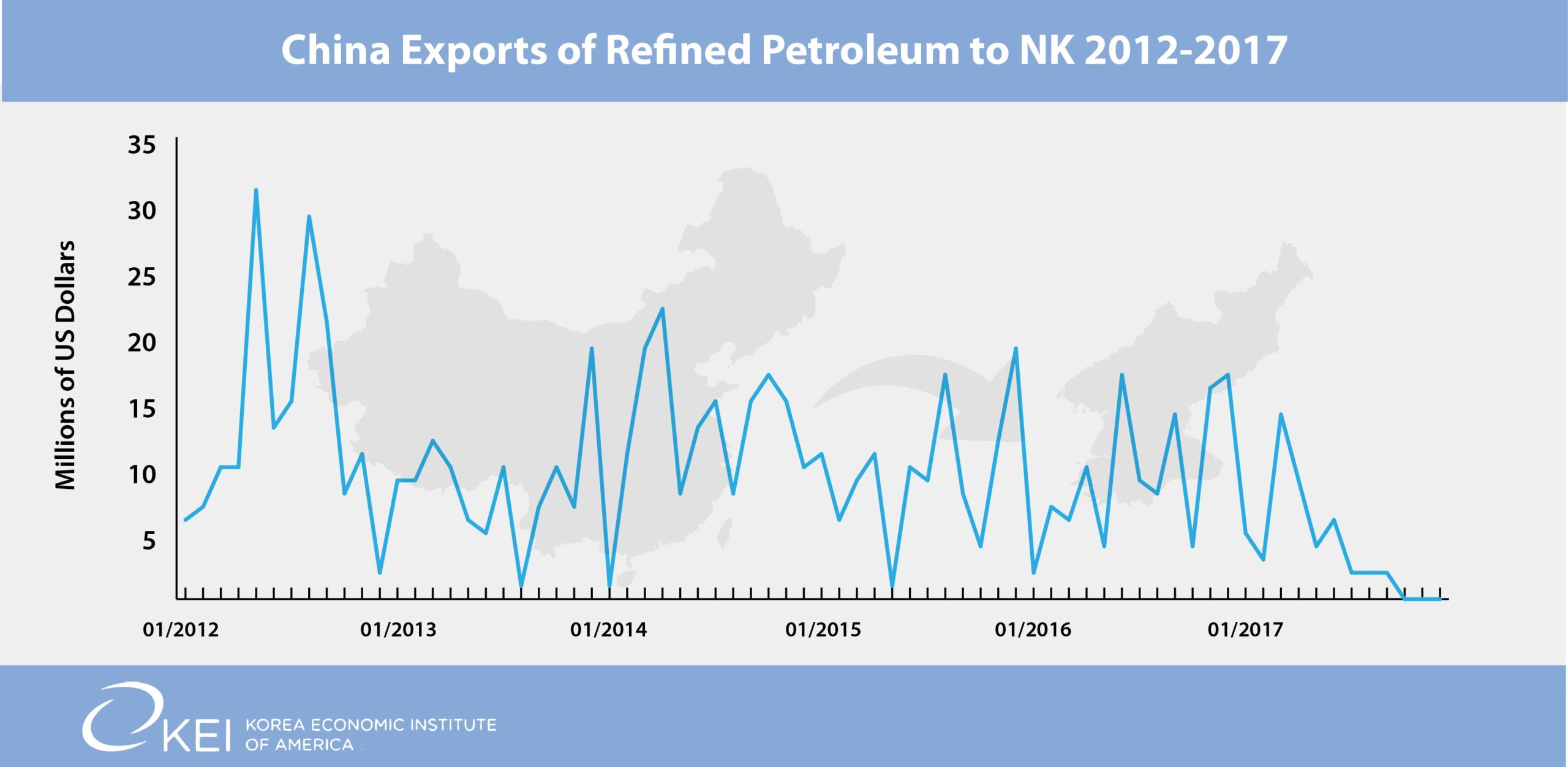

The detailed commodity data release shows, not surprisingly, a high degree of conformity to the UN Security Council’s increasingly tough sanctions, enacted in several increments since November 2016.[ii] Chinese imports of North Korea’s most valuable products; coal, lead, zinc, steel, iron ore, and fish, each registered zero in December and large drops for the fourth quarter and full year. Chinese exports are less constrained by the sanctions but, most importantly, shipments of petroleum products–gasoline, diesel fuel, and kerosene–fell to near zero. This means these important fuels must come from the country’s one operating refinery near Sinuiju, in the northwest corner of the country, that processes Chinese crude oil which apparently continues to be provided at historic rates, plus whatever shipments are obtained illicitly.

Interestingly, Chinese exports of consumer products, such as cell phones, sugar and confectionaries, fruits and vegetables, and milled grain have held up better than industrial products, such as coking coal used to make steel, and industrial equipment, possibly showing the resilience of North Korea’s relatively new consumer markets that import products from China and sell in US dollars or RMB. State firms that import industrial goods may be getting squeezed by a shortage of dollars; thus, their imports have dropped sharply, further bad news for an economy already relying on antiquated equipment.

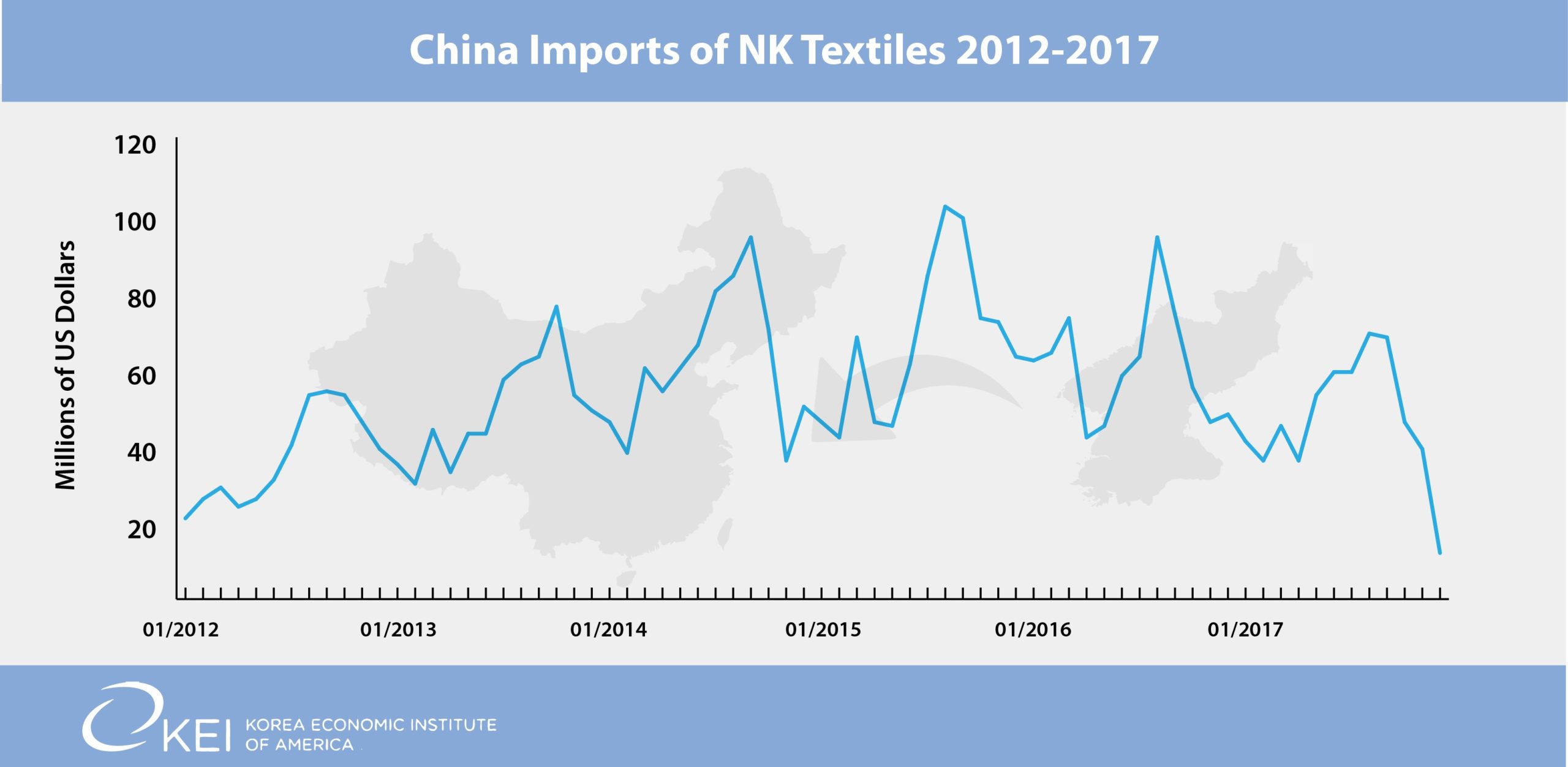

The newest big casualty shown in the December data is Chinese textiles imports. These were included in the September UN sanctions but with a phased reduction period, that is now biting. Textiles trade, both imports and exports, had grown in recent years to just behind coal as the most traded product, as Chinese and North Korean entrepreneurs took to joint venture deals and production arrangements to utilize North Korean plant and equipment, and cheap labor, to supply products for Chinese consumption and third country exports. New pilot policies set by Kim Jong-un, soon after he took power, allowed near market wages for production of export products, still very low by international standards but vastly higher than near-zero state wages, probably contributing to the growing textile trade. A big question now is what is happening to this industry, employing hundreds of thousands of North Korean women.

Another important question is how Pyongyang’s monetary authorities are managing to keep the North Korea won solidly pegged at W8,000 to the U.S. dollar, given widespread use of the dollar inside the country and the evident hard currency drain caused by the large trade deficit and similar draconian sanctions on the country’s external service earnings and remittances. An increased monthly outflow of $100 to $200 million on the trade account, compared to previous years, would be expected to cause a sharp drop in the value of the won, and consequent inflation, but so far it has not, according to Daily North Korea reporting through defector networks. Possible explanations each would require major trade-offs for Pyongyang authorities. Some of these include: government intervention in the small markets that buy and sell foreign exchange, although this would mean expending government, and likely Kim Jong-un’s own, foreign exchange reserves; severe restrictions on credit expansion by the central bank, although this would hurt state agencies and enterprises that try to invest or raise the wages of their extremely poorly paid workers; attempts by the regime to tax or raise fees wherever possible to bring in money, creating much grumbling among the population; or gradual liquidation of the state’s enormous capital assets, which include virtually all of the country’s land and much of its housing and industrial equipment. The latter might be the best choice for Kim, since in addition to providing funds, such privatization quickly raises worker and capital productivity, but it would likely put the country on a Chinese track for economic reform, something Pyongyang has strongly resisted now for three decades.

Data falsification and smuggling also may be playing a part—the actual deficit might not be as large as official data indicates–but anecdotal information suggests that this is not enough to make a large difference, especially to the North Korean state which would like have difficulty controlling illicit trade itself. Much has been made of illicit coal exports, for example, but one referenced ship that had transferred coal in the middle of the Yellow Sea carried only $1.5 million of the product, a small amount compared to monthly figures that averaged several hundred million dollars before last year. Costs for illicit trade are much higher than normal trade and falsification of data in China is dangerous and requires the cooperation of many actors, all of whom could be expected to be highly compensated for their risky actions.

The one area Beijing continues to resist challenging Pyongyang is the delivery of free crude oil, likely seen as the last big lever on Pyongyang, but even here China has agreed to quarterly limits that easily can be shrunk should Pyongyang engage in further provocations. Petroleum is already a very scarce commodity in North Korea and its not clear what it would do if China shut off the supply entirely.

With or without a crude oil shutoff, as China continues to ratchet up economic pressure via sanctions already in place, Kim may find himself facing a tough, even epochal decision, choosing between two dangerous alternatives; continuing the nuclear weapons program even as loss of export markets and foreign aid forces him to liquidate state assets and cave to Chinese-like reforms, or backing off the nuclear weapons development and hope, without guarantee, that eased sanctions and likely aid would allow him to restore essential elements of his father and grandfather’s Marxist command economy that he is on the verge of losing.

As someone said, Korea is a land of not-so-easy choices, for either side.

William Brown is an Adjunct Professor at the Georgetown University School of Foreign Service and a Non-Resident Fellow at the Korea Economic Institute of America. He is retired from the federal government. The views expressed here are the author’s alone.

Photo from Roman Boed’s photostream on flickr Creative Commons.

[i] All data is from Global Trade Atlas, using official Chinese Custom Bureau data.

[ii] See Asan Forum, November 2107, for a description of UN and US sanctions. http://www.theasanforum.org/sanctions-and-nuclear-weapons-are-changing-north-korea/