By Sunhyung Lee

Why South Korea’s Currency Is Weak Despite Strong Exports

New Bank of Korea Governor Shin Hyun Song faces a more constrained environment in shaping South Korea’s monetary policies.

Listen to this article

0:00 / 0:00

South Korea’s monetary elite hold portfolios that look a lot like the economy they oversee: global, dollar-exposed, and deeply tied to foreign markets. The foreign asset holdings of the new Bank of Korea (BOK) Governor Shin Hyun Song, disclosed during his confirmation process, are not an outlier. His portfolio reflects where Korean wealth is going, and how that trajectory is reshaping the won. Koreans are chasing foreign assets, especially U.S. assets, because they offer stronger perceived returns and a way to hedge against domestic uncertainty and won depreciation.

Korea is no longer just a country that earns foreign exchange through exports and then recycles it domestically. It is increasingly a country in which households, institutions, and firms actively allocate wealth to foreign assets. Koreans are now sending money abroad faster than the country earns from trade. Between January and November 2025, residents invested USD 129.4 billion overseas, while the current account surplus totaled USD 101.8 billion. That leaves the BOK to cover the roughly USD 27.6 billion gap out of its reserves. Markets read persistent outflows and repeated interventions as signals that the won will continue to weaken.

This shift changes how the won should be understood. Traditionally, movements in the won were often framed in terms of exports, imports, and trade competitiveness. But in today’s Korea, the exchange rate is increasingly shaped by portfolio behavior. When Korean residents buy U.S. stocks, foreign bonds, and overseas real estate at scale, they create steady demand for foreign currency. Even with a solid current account surplus, those capital outflows continue to put pressure on the won. This is why Korea can look strong in trade terms and still face a persistently weak currency.

Understanding the USD-KRW Exchange Rate

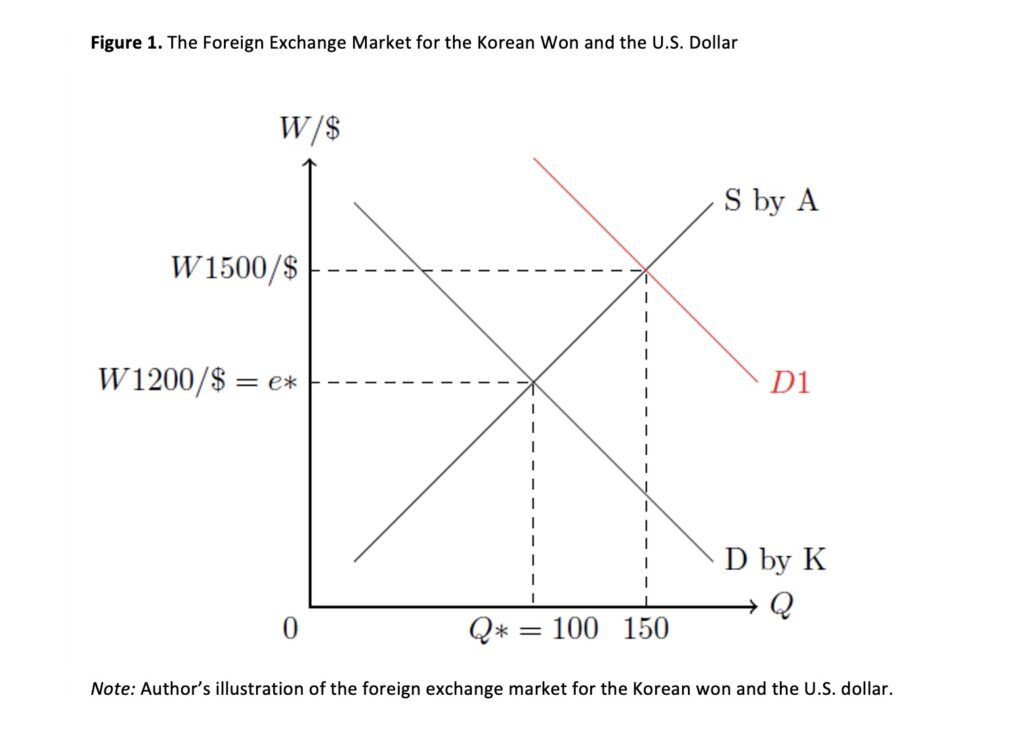

Figure 1 shows the foreign exchange market in its simplest form. When Korean investors buy U.S. stocks, bonds, and real estate at scale, they generate demand for dollars. That demand pushes the KRW-USD exchange rate higher regardless of inflation. A currency can look strong on trade fundamentals and still weaken because of where domestic investors are sending their money.

In exact terms, the KRW-USD exchange rate appears on the vertical axis (W/$)E, and the quantity of dollars on the horizontal axis (Q). The demand for dollars comes from Koreans (D by K) buying U.S. goods, services, and financial assets, while supply comes from Americans (S by A). Their intersection determines the equilibrium exchange rate and quantity (e*). Over the long run, that equilibrium is tied to purchasing power parity: the relative buying power of the won and the dollar. But short-run exchange rates can move for reasons unrelated to inflation. Suppose the market begins at KRW 1,200 per USD. If Korean investors increase their purchases of foreign stocks, demand for dollars shifts outward (D1). The result is a higher exchange rate, say KRW 1,500 per USD, which means the won has depreciated. Even with no changes in inflation differentials, portfolio decisions alone can weaken the won in the short run.

For monetary policy, this means the BOK operates in a more constrained environment than before. The policy rate cannot solely be set with domestic growth and inflation in mind—it must also account for cross-border capital flows and financial stability.

That makes the interest rate question more difficult. If growth slows, the textbook answer may be to cut rates. But if residents are already sending large amounts of capital abroad and the won is under pressure, rate cuts risk intensifying depreciation and adding to inflation. On the other hand, keeping rates higher to protect the currency may come at the cost of weaker domestic demand. This is exactly the environment the BOK now faces. At its April 10, 2026, meeting, it kept the base rate unchanged at 2.5 percent, explicitly citing high uncertainty, upside inflation pressure, downside growth risks, and heightened volatility in financial and foreign exchange markets. It remains to be seen how the next meeting on May 28, with Shin at the helm, may depart from this.

Conclusion

Regarding both the Korean economy and how the new BOK governor is slated to govern, Korean money now moves across borders on a scale large enough to shape the won. The portfolios of BOK officials reflect that transformation rather than stand apart from it. That is precisely why the next phase of Korean monetary policy will be so challenging: the central bank must manage inflation, growth, and financial stability in an economy where domestic wealth is increasingly global and where the exchange rate is driven as much by asset allocation as by trade.

This does not mean Korea’s central bank lacks credibility or that foreign asset holdings by central bankers automatically compromise its integrity. But it does mean the debate matters for reasons larger than ethics alone. It reveals how deeply Korea’s financial life is now tied to global markets, and how much harder monetary policy becomes when the won is shaped not just by exports and inflation, but also by Koreans’ outward investment decisions.

That challenge becomes even more complicated when Korea’s monetary policy decisions are viewed alongside uncertainty over the future direction of U.S. interest rates, with Kevin Warsh expected to become the next Federal Reserve chair. Markets may anticipate a greater likelihood of U.S. rate cuts, but cutting rates in a still-inflationary environment would not be straightforward. For the BOK, this adds another external variable to an already difficult policy calculus, forcing the governor and board members to weigh domestic inflation, growth, exchange rate pressures, and the uncertain path of U.S. monetary policy.

Sunhyung Lee is a Non-Resident Fellow at the Korea Economic Institute of America (KEI) and an Assistant Professor of Economics at the Feliciano School of Business, Montclair State University. The views expressed are the authors’ alone.

Feature image from Hyun Song Shin’s X account.

This material is distributed by KEI on behalf of the Korea Institute for International Economic Policy. Additional information is available at the Department of Justice, Washington, DC.