Political Turbulence Clouds South Korea’s Economic Outlook

The additional concerns about political instability have led some forecasters to downgrade their outlook for Korea in 2025.

South Korean President Yoon Suk Yeol’s short-lived declaration of martial law on December 3, 2024, and his subsequent impeachment on December 14 have plunged the country into its worst political crisis in nearly 40 years, with some signs of a negative economic impact. The economy was already showing signs of weakness before the December political crisis. In particular, industrial production decreased in November 2024 for the third consecutive month. The additional concerns about political instability have led some forecasters to downgrade their outlook for Korea in 2025.

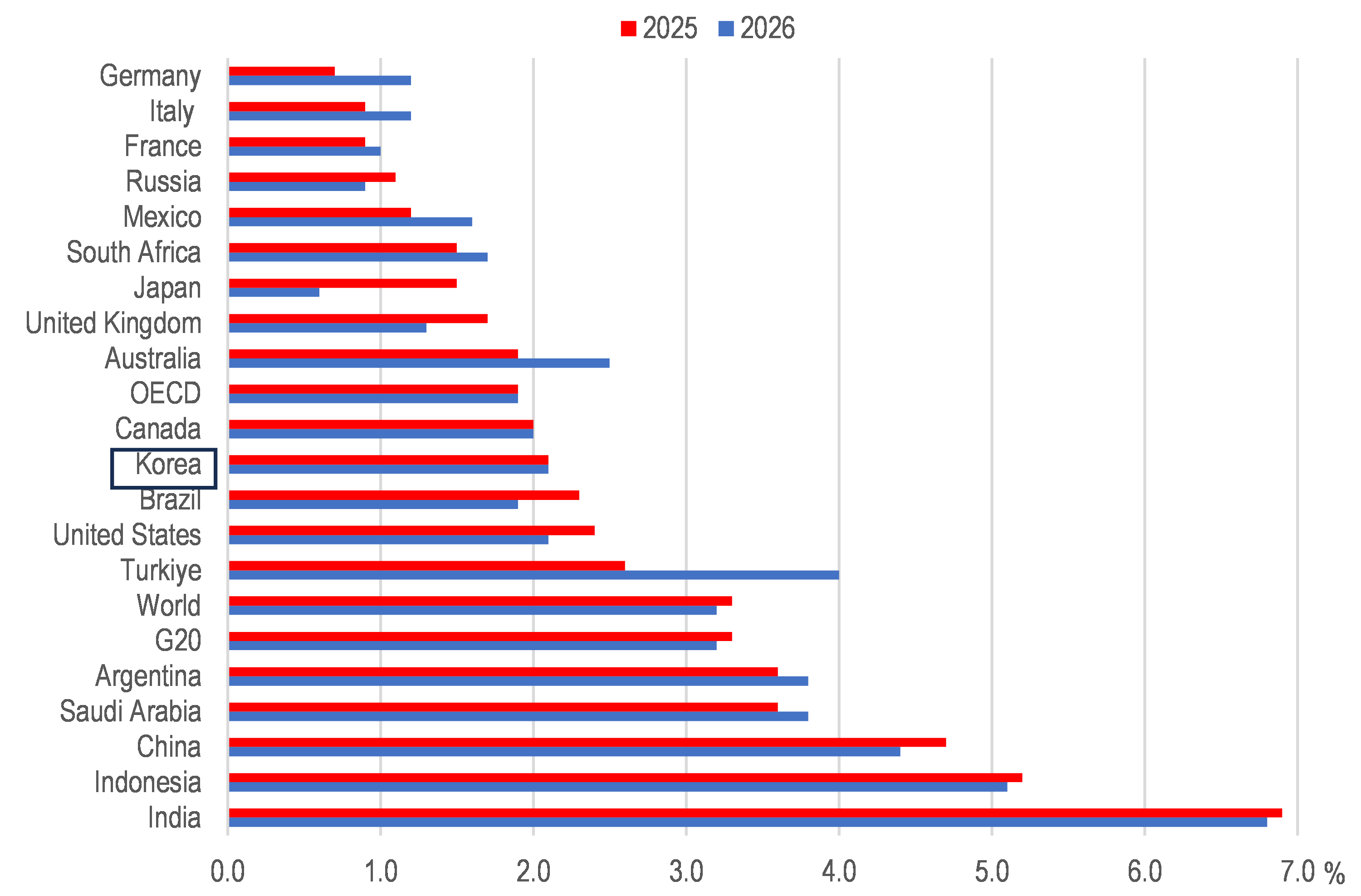

Economic Growth Projection for Korea in 2025

The OECD Economic Outlook, published on December 4, projected that Korea’s real GDP would increase by 2.1 percent (Figure 1) in 2025 despite signs of weakness during 2024. Indeed, GDP declined slightly in the second quarter last year, followed by only 0.1 percent growth in the third. Strong global demand for Korean products, notably semiconductors, drove growth in the first half of 2024, but exports declined in the third quarter. The 2025 OECD projection is down slightly from the expected 2.3 percent in 2024 and is in line with Korea’s 2 percent potential growth rate (the rate an economy can sustain at full capacity utilization and full employment). The OECD projection aligns with the 2.0 percent forecasts made last November by other institutions, including the IMF and the Korea Development Institute.

Figure 1. OECD projections for the G20 countries in 2025 and 2026

Source: OECD Economic Outlook, Volume 2024 Issue 2.

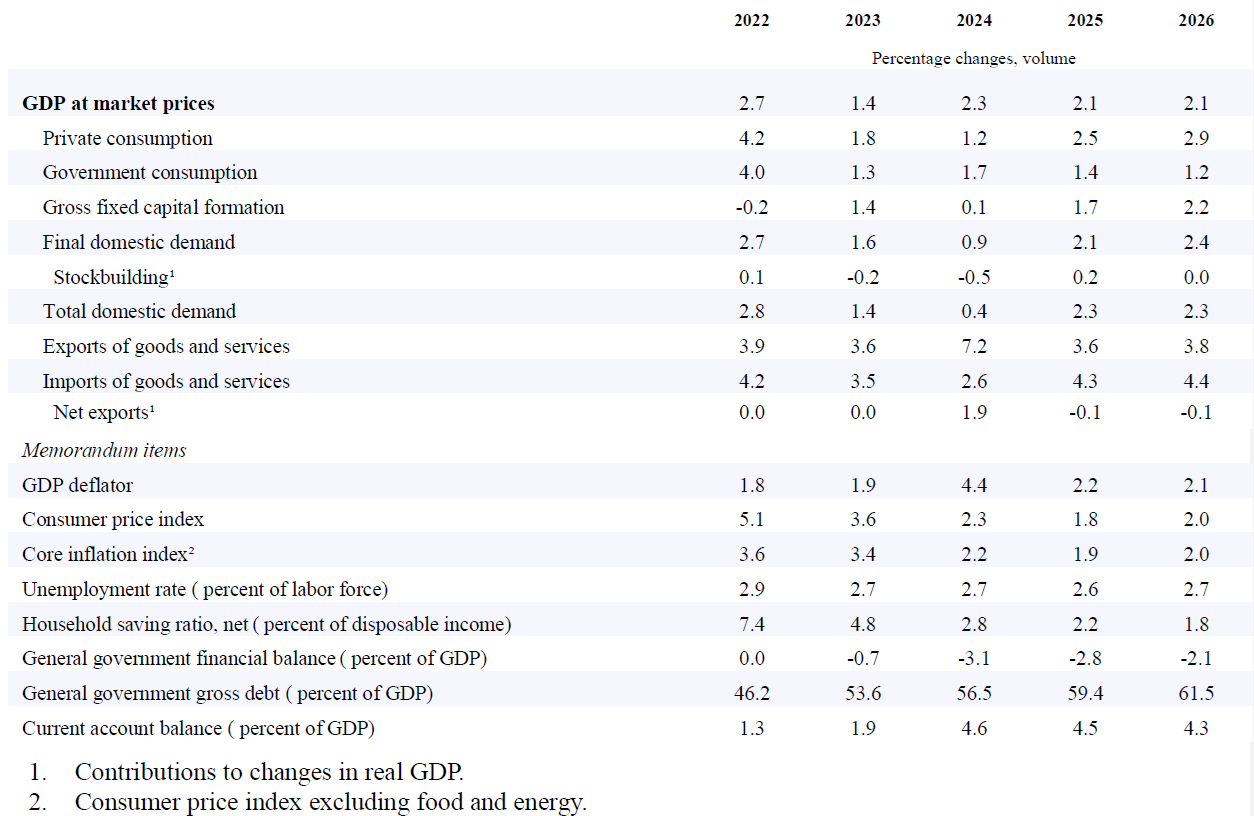

The OECD expects investment and private consumption to drive growth, as cuts in the Bank of Korea’s policy interest rate and real income gains boost purchasing power (Table 1). Further increases in the labor market participation of women and older persons will boost the employment rate, which reached a historical high of 62.7 percent last October. The unemployment rate is expected to remain low at only 2.7 percent, with continuing labor shortages in sectors such as shipbuilding and health. Export growth is projected to remain below 4 percent in both 2025 and 2026.

Table 1. OECD projections for Korea in 2025 and 2026

Source: OECD Economic Outlook, Volume 2024 Issue 2.

Economic Impact of Political Uncertainty

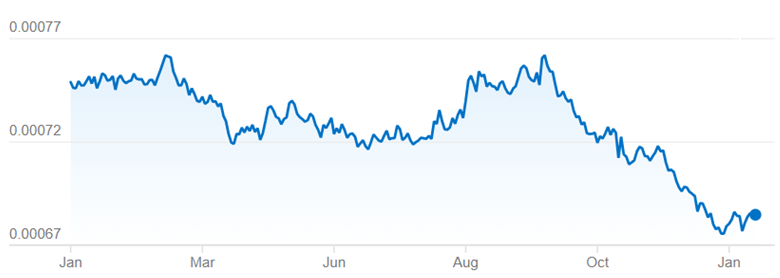

One immediate impact related to the political events last December was the decline in the USD/KRW exchange rate. By mid-January, it had fallen by about 3 percent from its level on December 3, leaving it 10 percent below its peak in late September (Figure 2). On January 16, Bank of Korea Governor Rhee Chang-yong stated, “Political changes sparked by the martial law imposition have greatly affected the foreign exchange market.” He added that the won was weaker than expected based on economic fundamentals.

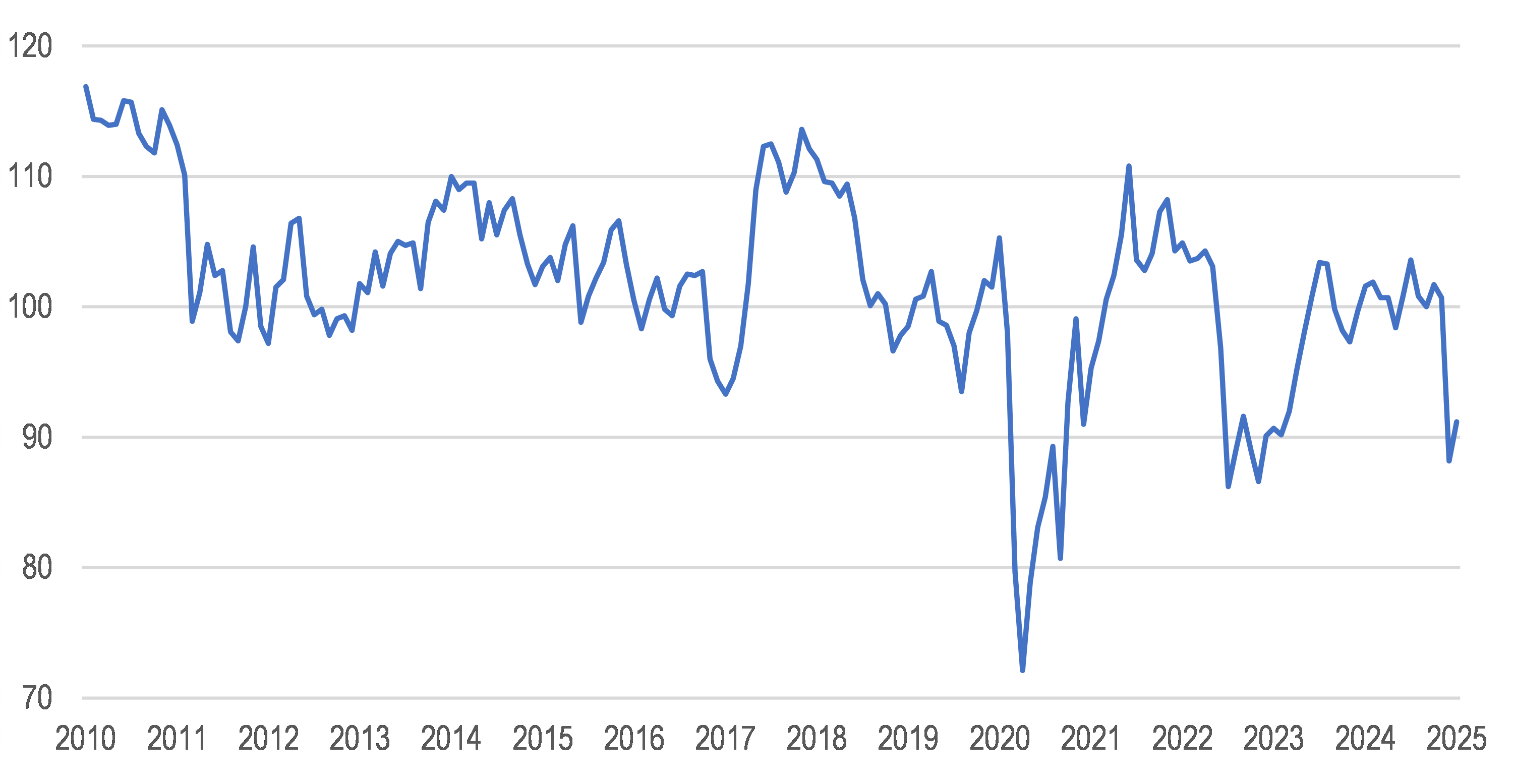

Consumer confidence, which is closely linked to private consumption, has also taken a significant hit. The Consumer Sentiment Index (CSI), which measures consumers’ optimism about the economy, fell sharply in December 2024 (Figure 3). However, it was not as severe as the pandemic-related shock in 2020, when private consumption dropped by 5 percent. Moreover, it increased in January 2025. Still, the overall decline between November and January exceeded that recorded during the three months leading up to the impeachment of President Park Geun-hye in January 2017. Indeed, the CSI fell to a lower level in December 2024 (91.2 versus 93.3 in 2017) and by a larger amount (10.5 points versus 9.4).

Moreover, the Business Survey Index (BSI) of the country’s top 1,500 manufacturing companies (based on their sales) stood at 88 for the first quarter of 2025, down from 95 during the fourth quarter of 2024, according to the Korea Institute for Industrial Economics & Trade (KIET). A reading below 100 means pessimists outnumber optimists. In December, Korea lost 52,000 jobs from a year earlier, the first year-on-year decline in employment in nearly four years. Real GDP in the final quarter of 2024 increased by only 0.1 percent (quarter-on-quarter), the same rate as in the third quarter. For the year 2024, real GDP expanded by a weaker-than-expected 2.0 percent. The Ministry of Economy and Finance’s monthly economic report (the Green Book) in January 2025 stated, “Recently, our economy has faced increasing downward pressure on growth and weaker employment due to expanded uncertainties at home and abroad.”

Figure 2. The won has fallen relative to the dollar

The daily dollar-per-won rate since the beginning of 2024

Source: Refinitiv, Thompson Reuters.

Figure 3. Korea’s Consumer Sentiment Index plunged in December 2024

Source: Bank of Korea.

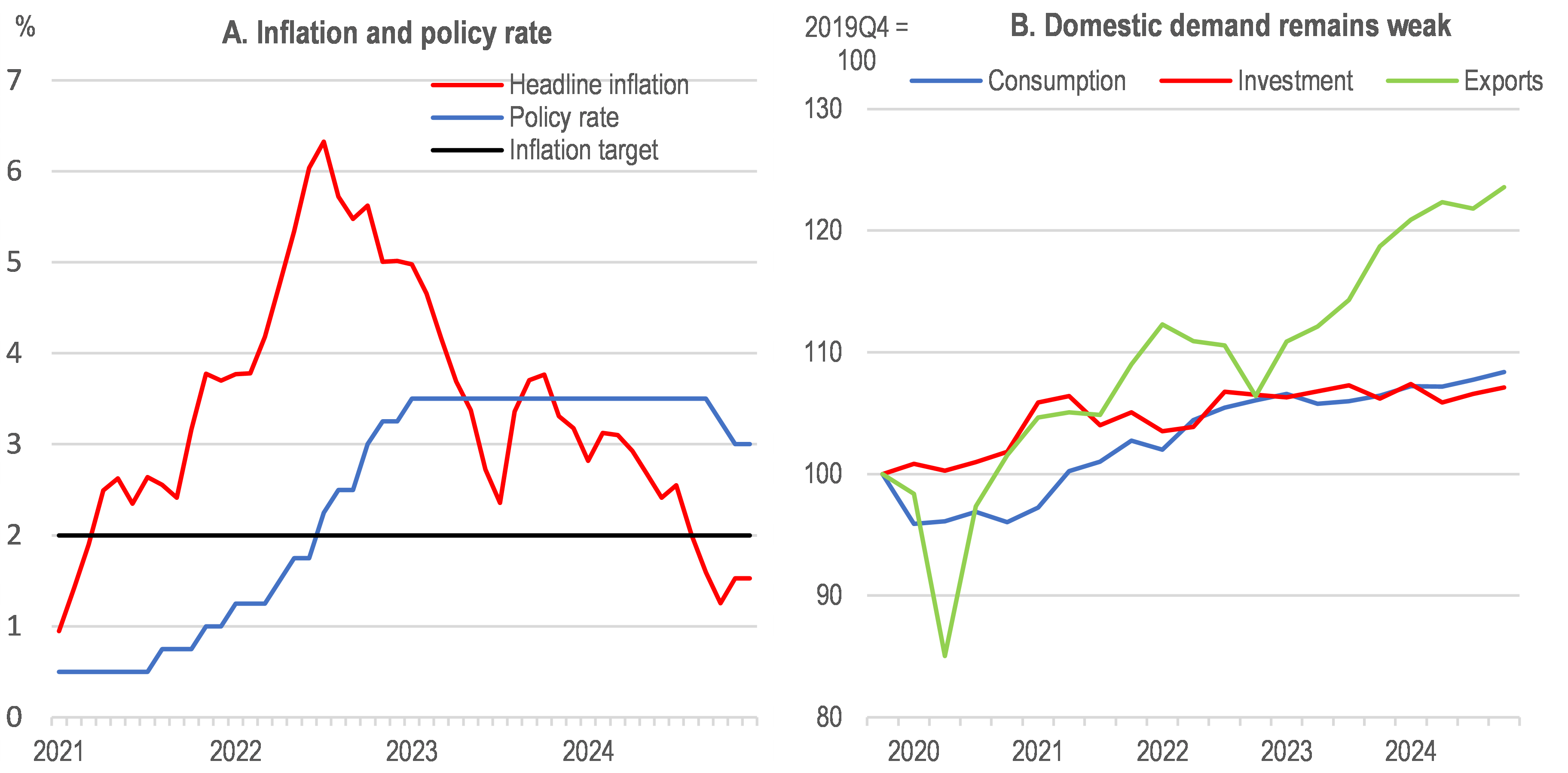

A more medium-term impact of Korea’s political turbulence and the resulting fall in the exchange rate is its influence on monetary policy. With the inflation rate falling below the 2 percent central bank target, the Bank of Korea cut its policy interest rates to 3 percent in two steps during the final quarter of 2024 (Figure 4, Panel A). Given weaker economic growth, the Bank of Korea stated that another interest rate cut was warranted. However, the Monetary Policy Board meeting on January 16 kept the interest rate unchanged at 3 percent, citing the weak local currency. Lower interest rates would help boost private consumption (about half of GDP) and investment, which have only risen around 8 percent since the final quarter of 2019, while exports increased 24 percent (Panel B).

Figure 4. Inflation fell below the 2 percent target, while domestic demand remains weak

Source: OECD Economic Outlook, Volume 2024 Issue 2.

Following the declaration of martial law and the impeachment of President Yoon, some institutions have become less optimistic about Korea’s economic prospects for 2025. For example, the Hyundai Research Institute cut its projection from 2.2 percent to 1.7 percent. The Bank of Korea likewise lowered its forecast from 1.9 percent to 1.6-1.7 percent. Following the January Monetary Policy Board meeting, Governor Rhee noted, “The drop in domestic demand, especially regarding consumption and construction contraction, has been more significant than we have initially expected.” Weak growth since the second quarter of 2024 and political uncertainty raise doubts about Korea’s ability to sustain a 2 percent growth .

Conclusion

Political stability is closely tied to Korea’s economic prospects in 2025. Political uncertainty has also led the Yoon administration to significantly scale back its deregulation agenda and reform initiatives, negatively impacting the country’s growth potential over the medium term. Resolving the political impasse would help improve consumer and business sentiment and reduce downward pressure on the exchange rate, opening the way for interest cuts to support economic growth. At the same time, the government budget implies a fiscal tightening of about 1 percent of GDP during the 2025-2026 period, according to the OECD. The Ministry of Economy and Finance announced that it plans to allocate three-quarters of the 2025 total fiscal budget during the first half of the year to support the economy. If political uncertainty continues, the government may need to slow the pace of fiscal tightening to sustain economic growth. Acting President Choi Sang-mok said in early January that the government will consider additional measures to stimulate the economy in the first quarter of 2025 if necessary. The main opposition Democratic Party has called for a supplementary budget of at least 20 trillion KRW (13.7 billion USD, 0.8 percent of GDP).

Randall S. Jones is Distinguished Fellow at the Korea Economic Institute of America. The views expressed here are the author’s alone.

Photo from Shutterstock.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.