Is Tight Money and Sanctions Driving North Korea into Depression?

By William Brown

It is an odd question, but it may have a lot to do with the current quandary over whether or not to provide food aid to an incalcitrant but hungry country. And even more importantly, on how to induce Kim Jong-un back to the table for real negotiations.

We don’t normally pay much attention to North Korea’s monetary or fiscal policies. After all, the communist state prides itself on its Marxist or command economy system, a system in which money, and interest rates, should play nothing of the determinative role they play in a market economy. Prices are fixed in accordance with policy desires, everything is allocated by the state and Party through a massively complex central plan, and pay is by ration tickets, not money. Interest isn’t charged or collected—after all that would mean money making money. Central bank notes circulate as if they are money, but their role is limited to accounting instruments, and are as plentiful as they are worthless. And not lost on the Stalinist state, people without money are much easier to control than people with independent wealth.

But this is the theory of North Korea, not today’s reality. The central plan mechanism never really worked well, the military sapped the resources saved by weak consumption, and industry was built only with massive amounts of aid from the Soviet bloc and China[1], and later by aid and extensive borrowings, never repaid, from Western Europe, Japan, South Korea and even the United States.

During the famine of the mid-1990s, the state couldn’t provide food rations and the command system and the plan broke apart. Instead of rations, the already plentiful won notes began to circulate as money, and the state printed more, eviscerating their value in two decades of hyperinflation.[2] Foreign money, Chinese yuan and U.S. dollars, began to seep in and now circulate in tandem with the won notes, a rare, partially dollarized monetary system. Kim Jong-un, for all his inexperience, surprisingly has managed to stabilize the won by allowing the foreign money to circulate without restriction, effectively ending capital controls and creating in some ways a liberalized capitalist-like economy, only without legally protected property rights. One might say North Koreans have transitioned from ration tickets, to worthless money, to an odd form of hard currency capitalism in one generation.

Understanding how and why this has happened, especially in the face of the current severe sanctions that one would have thought would have collapsed the won is essential to understanding the current pressures on the regime. In my view these pressures are very strong and likely occupy most of the government’s time and energy. If the nuclear and other humanitarian issues we have with North Korea are to be resolved, we need to understand what Kim and others in North Korea are dealing with on their domestic plates. They may be more important to the regime’s security than are the nuclear weapons.

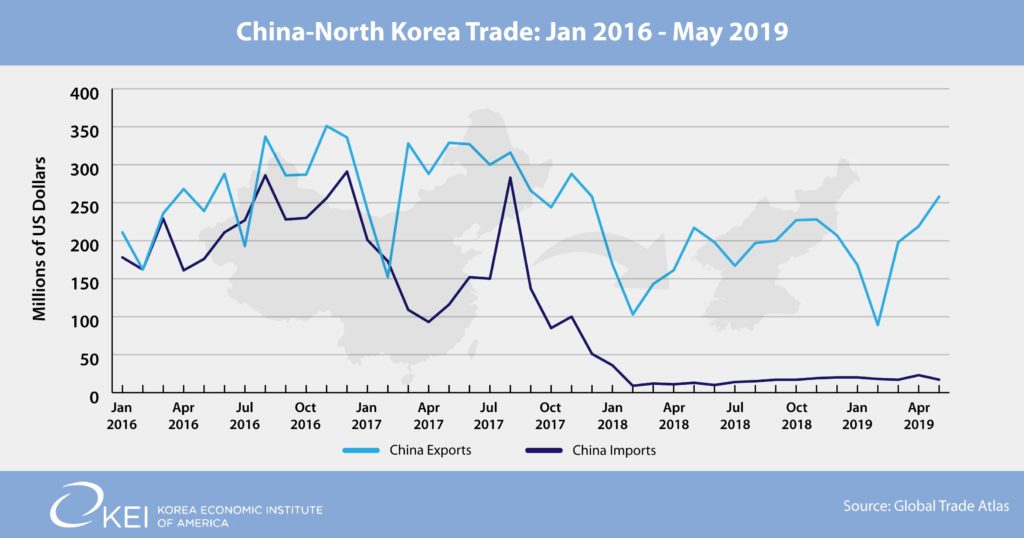

The collapse in exports must be devastating. Just released data by China’s customs bureau show imports from North Korea, that is North Korean exports, in the year through May totaled only $95 million, up slightly from 2018 but only a fraction of the $692 million in the first five months of 2017, before the UN sanctions really came into force. China’s exports through May rose slightly to $932 million but were down from $1.3 billion in 2017. China’s surplus, Pyongyang’s deficit, continues to rise, at $836 million in the year through May. [3]

The resiliency in North Korean imports, despite the loss of export revenue, is interesting, driving up the goods trade deficit, but the commodity composition tells a larger story. Imports of all kinds of industrial and investment goods have collapsed whereas imports of consumer goods have remained steady, even increasing. The former are bought by the state and its enterprises, the later by the public and sold in markets. And new, non-sanctioned items, are soaring. Watch parts, for instance have gone from essentially nothing in 2018 to become the largest North Korean export commodity and is supported by a huge increase in imported watch parts. And the strength shown in consumer goods imports, including many foodstuffs, may be helping control market prices. In effect, a decline in government spending on imports of investment goods may be supporting the consumer, at least for now.

In the face of this soaring goods trade deficit, many are asking how Pyongyang maintains its currency stability. There are not too many possibilities. Our data could be wrong and the won is much weaker than defectors’ organizations report, exports really are not as decimated as China and other trade partners report, services and transfers income is much larger than has been estimated and is growing to offset the rising goods deficit, or someone is pumping huge amounts of investment dollars or aid into North Korea without letting the rest of the world know. Lastly, the country may be drawing down foreign exchange reserves at a rate that over months or a few years will dry up all privately and state held dollars and yuan and the population doesn’t know or understand the forces at play—dangerous because once they figure out the outflow there could be panic selling of won and a crisis for the regime, much worse than a similar episode in 2009.

Some of all the above are likely at play but in my view do not account for all of the increase in the goods deficit. If so, this would seem to require, at least theoretically, an extremely tight won policy as the regime’s only policy choice. As with a currency board, every outflow of hard currency is matched with a withdrawal of won money from circulation, keeping the balance between won and hard currency stable. This would mean no fiscal deficits that would flood the country with won and a severe cutback in new won-denominated loans to state enterprises, again removing won from circulation as loans are repaid, keeping won as scarce as the ever-decreasing supply of U.S. dollars and Chinese yuan.

If this is correct, Kim is buying stability by shrinking the economic role of the state. Instead of loans or needed state wage increases, authorities are allowing state enterprises and employees to sell or lease state property and, probably more importantly, allowing private use of state property and licenses. Tax increases could play the same role but the country lacks an effective tax system. Fees, however, do seem to be increasing. A big advantage of the tight money is that the public is learning to trust the won on a day-to-day basis and thus chooses not to speculate against it. And increasing privatization is allowing productivity growth that may offset the downturn in the state sector. But the authorities clearly are not yet confident enough of this trust to try to force the public to turn in their dollars for won and get rid of the troublesome dollarized system.

Dollarization is troublesome for any state because it reduces or even eliminates the ability of authorities to create new cash money, advance credit or, as in the case of North Korea, even to run a fiscal deficit using borrowed money. It is like a U.S. state with a balanced budget requirement and a terrible bond credit rating, or like a currency board economy, like Hong Kong, where domestic money can be created only when U.S. dollars have been accumulated, either through an increase in exports, a reduction in imports or a net increase in inward foreign investment. Except unlike Hong Kong, North Korea is under huge worldwide sanctions pressure on its trade.

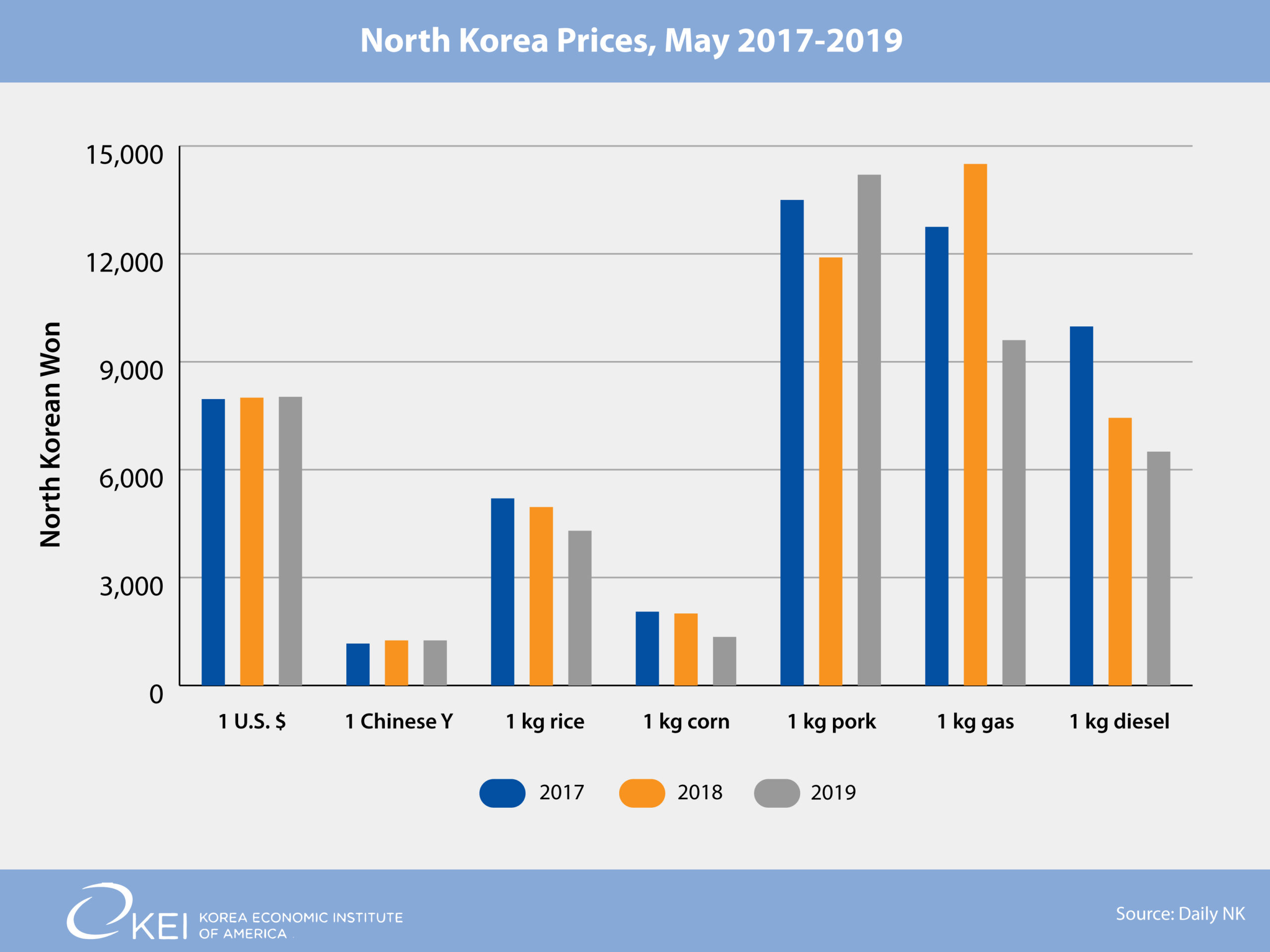

Tight money and a related recession could mean prices are deflating, presenting a new problem for the recently thriving market economy, especially for the merchants and for anyone who has borrowed money to buy real assets. The asset price would have declined, and the loan would have to be paid back in won that was more valuable than had been expected. Bankruptcies, and unemployment in the market sector, would be rising among millions of people with no social safety net. And evidence from defector sources, as published by DailyNK, suggest this may be the case. Market observers say there is plenty of products in markets, but no one has money to buy, so prices are falling. Similarly, apartments, which were sold at high values last year are now worth much less—legally such private property is not allowed but a vast grey market has developed over the past ten years with Pyongyang apartments changing hands for $30,000 U.S. dollars, or more. Tight money may be lowering the price of rice and corn even as the country suffers from a weak harvest last year, a sign of depression rather than a sign of plenty.

Dealing with deflation is in some ways harder for a government than is dealing with inflation, as Japan has learned over the past two decades. Kim’s focus in Hanoi was on sanctions relief. But what he really may need is to build a new monetary system. If so, Trump could offer a lesson in how the U.S. helped South Korea do just that in 1962, setting the country off on a record setting growth path.

William Brown is a non-resident scholar at KEIA and teaches at Georgetown University and UMUC. This and other related postings can be found on his website, NAEIA.com

Graphics by Juni Kim Program Officer at the Korea Economic Institute of America.

Photo from NVictor’s photostream on flickr Creative Commons.

[1] Chinese aid to North Korea has normally been in the form of crude oil and other commodities, with a rare power plant or smaller factory thrown in.

[2] 2.16 won was equal to a US dollar in the 1970s. (Said to be set by Kim Il Sung’s birthday, Feb 16.) By 2015 it would take 820,000 won (2 zeros were added in 2009) to equal a dollar. But that rate has held essentially even now for about five years, a notable achievement for Kim Jong-un but at a cost to the economy.

[3] The data is not seasonally adjusted so fluctuations, especially in the winter months, are exaggerated. The mid-2017 upturn in Chinese imports is due to a lagged impact of coal sanctions—the physical imports occurred earlier in the year but sat on docks until Beijing allowed customs clearance in August, prior to slamming on the brakes. The Chinese export data wrongly does not include crude oil transfers by China totaling about 41,000 tons (292,000 bbl.) a month, worth about $17.5 million. As with the U.S. Agreed Framework heavy fuel oil, and South Korean grain shipments, these are probably loans that are not expected to be repaid.