How South Korean Investment Brings Latent Capacity to U.S. Naval Power

Where U.S. domestic industrial capacity has withered, foreign investment could intervene to halt further degradation of the U.S. shipbuilding industry.

By Andy Hong

For the first time in decades, there is a real sense of urgency in revitalizing U.S. shipbuilding. There is bipartisan political interest in challenging China’s dominance in this space, and the U.S. private sector appears poised to capitalize on the momentum. Tangible and well-timed developments such as Hanwha’s purchase of Philly Shipyard have added to the perception that tides are changing for the much-maligned U.S. shipbuilding industry. Further investments from and partnerships with allies like South Korea and Japan will continue to drive the restoration of shipbuilding in the United States.

But much needs to happen before any dramatic increase in the output of hulls leaving U.S. slipways is possible. Commercially, the U.S. industrial base is too atrophied, and the global market is too saturated for the United States to once again become a dominant shipbuilder without some seismic shift in the industry. In naval building, regulatory limitations on sensitive technologies and procurement inefficiencies dampen hopes that allied shipbuilders would produce U.S. naval combatants and auxiliaries in the near future. Yet, instead of being discouraged, it is important for advocates and policymakers to remain clear-eyed on the most immediate—but also critical—benefit that foreign investment brings.

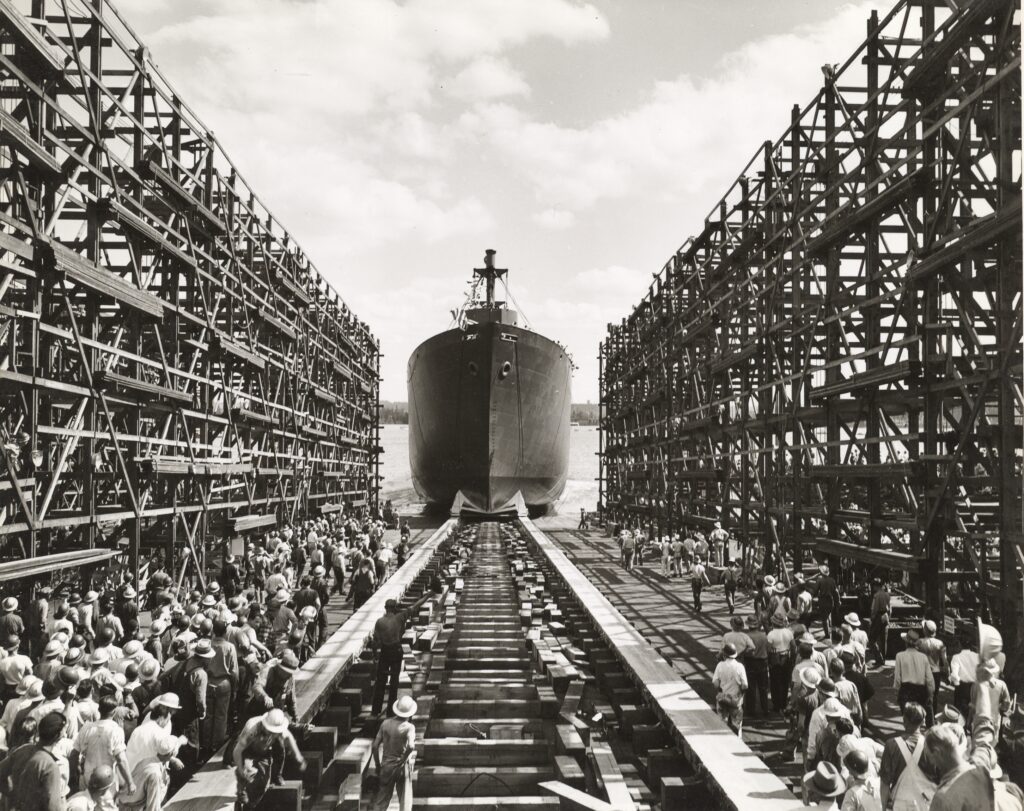

Crucially, South Korean investment in U.S. shipyards can help stem the loss of latent capacity by keeping shipyards open and skilled labor employed. The U.S. shipbuilding industry is in such poor straits that stopping further damage is a valuable first step while also being a more attainable objective than outcompeting competitors like China. Foreign investments from South Korea keep docks open that would otherwise be forced to close. Shipbuilders, dockhands, and other highly skilled Americans employed at or because of the shipyard continue to hold their jobs. The machinery remains oiled and functional. These results may seem obvious and even inadequate if they do not translate to more hulls in the water, but keeping the infrastructure intact contributes to maintaining latent capacity in shipbuilding for the United States.

This latency means that the increase in shipbuilding capacity may not be immediately visible. Most domestic shipyards are geared toward naval manufacturing in the U.S. shipbuilding market. Meanwhile, most foreign-owned shipyards would likely focus on civilian vessels. It is true that South Korean firms like Hanwha recently made headway in meeting the requirements to partake in U.S. naval shipbuilding. Yet, when firms such as Fincantieri Marine Group clear the arduous regulatory hurdles and receive contracts from the U.S. Department of Defense, inefficiencies in U.S. military procurement mean that most shipyards do not regularly contribute to active naval industrial capacity, especially in peacetime when demand for naval shipbuilding tends to be low. When demand does increase, latent capacity contributes to U.S. strategic needs by providing the workforce and infrastructure necessary to respond to that demand. In security contingencies that could see a sudden need for greater shipbuilding capacity—whether in repairing damaged vessels or replacing lost ones—U.S. naval shipbuilders will face considerably lower pressure than if there were no other available shipyards with functioning machinery and trained laborers.

History demonstrates the strategic necessity of retaining such capacity. As World War II demonstrated, the United States must rely on more than its technical and martial superiority on the battlefield. Not unlike the U.S. Navy today, the Imperial Japanese Navy boasted highly experienced officers, advanced vessels, and modern tactics, parts of which would define naval combat for the rest of the century. The Allies suffered heavily as a result, including between August 1942 and February 1943, when U.S. and Allied navies lost three times more sailors off the coast of Guadalcanal than their peers ashore in the Army and Marine Corps. While matched on the seas against Japan, this type of prolonged, attritional warfare leveraged the one overwhelming advantage that the United States had: industrial capacity.

After each engagement, losses mounted on both sides. The United States could repair damaged vessels and replace sunken ones; its adversaries could not. Even Great Britain, with its vast colonial resources, was unable to effectuate repairs at the same rate, but the United States could keep the Royal Navy afloat with its excess capacity. Japan had focused its limited industrial capacity on building combatants, which led to an inability to recover from the collapse of its merchant marine and the starvation of its soldiers abroad. Meanwhile, the immense U.S. commercial shipbuilding industry ramped up both naval and civilian building, constructing thousands of vessels for the global war effort. Despite the Japanese successes and the U.S. setbacks from the attack on Pearl Harbor through the Solomon Islands campaign, the contest in the Pacific was decided in favor of the side more prepared for a total war between industrial powers. In this overarching sense, the skillset of each sailor and the quality of each vessel were immaterial to the ultimate outcome. The Pacific War was won not on aircraft carriers and oilers but on cranes and dockyards.

Today, that advantage no longer lies with the United States but with its chief maritime competitor, China. While the advent of nuclear weapons, long-range missiles, and unmanned vehicles will change the complexion of any potential future conflict, the basic premise of naval power holds that the side better able to recover from losses and damages at sea will be afforded greater strategic flexibility and tactical initiative.

Where U.S. domestic industrial capacity has withered, foreign investment could intervene to halt further degradation of the U.S. shipbuilding industry. Fortunately, the United States’ capable network of allies remains a key asset and advantage over its adversaries. Upholding partnerships with capable shipbuilding nations—South Korea, Japan, Italy, France, and others—will be critical to the revitalization of U.S. shipbuilding and the maintenance of maritime security.

Andy Hong is Program Officer at the Korea Economic Institute of America. The views expressed here are the author’s alone.

Photo from Wikimedia Commons.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.