Search All Site Content

Total Index: 6325 publications.

Subscribe to our Mailing List!

Sign up for our mailing list to keep up to date on all the latest developments.

The Peninsula

Provoking the Market: North Korea’s Impact on the South Korean Economy

By Kyle Ferrier

North Korean provocations are generally accepted to have a minimal impact on South Korea’s economy, yet in early 2016 these geopolitical risks have corresponded with losses in Seoul. South Korea’s stock exchanges, tracked by the KOSPI Index, closed 0.26% lower on January 6, the day of the claimed hydrogen bomb test, but this decline has largely been attributed to the largest devaluation of the Yuan in five months. The KOPSI also lost 2.93% on the first trading day after North Korea’s February 7 long-range missile launch, the largest drop ever on the first day the stock market could react to a North Korean long-range missile launch or a nuclear test. However, the South Korean government was quick to point out investors were not reacting to North Korea, but rather to slow global growth also precipitating massive selloffs in other major stock markets (February 12 closed the largest weekly drop in the Nikkei since the financial crisis and the Dow closed at a two-year low on February 11). Based on conventional wisdom, the relationship between the latest geopolitical developments and these financial losses is likely a mere coincidence, but to what extent should these incidents be considered as wholly isolated from market trends or at least marginally interconnected?

Though it is difficult to arrive at a concrete answer given the plethora of factors that influence the numerous daily transactions tracked by the KOSPI, the key to understanding North Korea’s current impact on the South Korean economy is to observe how this relationship has developed over time. The following sections look at financial data, specifically changes in the KOSPI quotes and South Korean won/US dollar exchange rate, on fourteen separate dates which correspond to major security developments in North Korea. These dates are grouped according to the similar qualitative aspects of their corresponding event: nuclear tests, engagements along the DMZ, and long-range rocket launches. These dates are by no means a comprehensive list of every time geopolitical risk stemming from North Korea has translated to economic losses in Seoul nor does public data allow for thorough intraday analysis. Nevertheless, the general conclusions that can be drawn from past data provide a better understanding of the current state of affairs and can provide insights into how markets will react to future geopolitical developments.

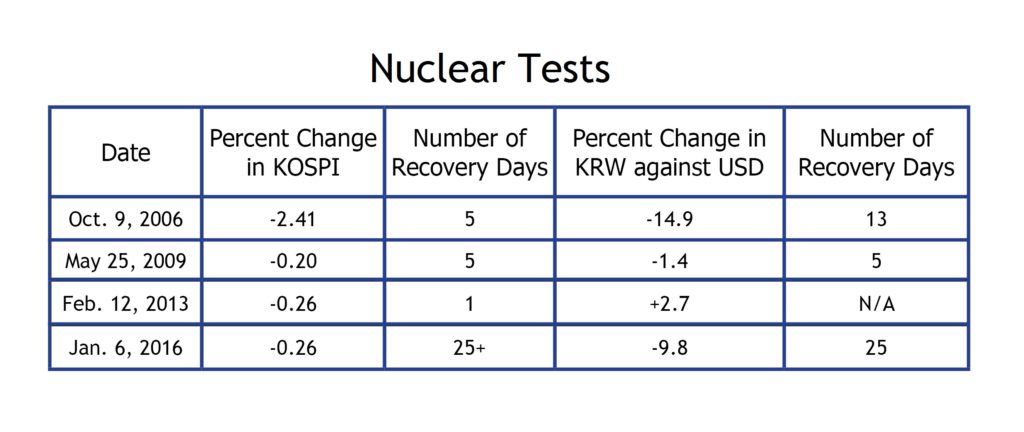

Nuclear Tests

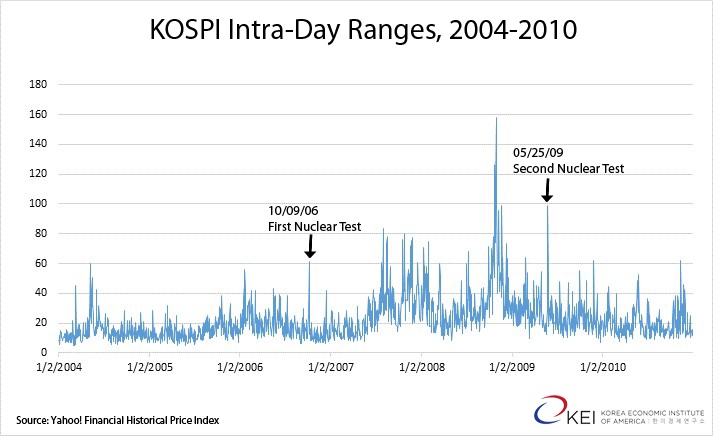

The first nuclear test in 2006 clearly had a much greater impact on South Korean financial markets than other nuclear tests, which is rather unsurprising as it represented the most precipitous change in the status quo. The 2006 test first demonstrated to the world that the rogue state would brashly pursue a nuclear program in spite of international opposition and a formal commitment to denuclearize. The second test in 2009 saw the smallest drop in the KOSPI of the four tests, but this is misleading.

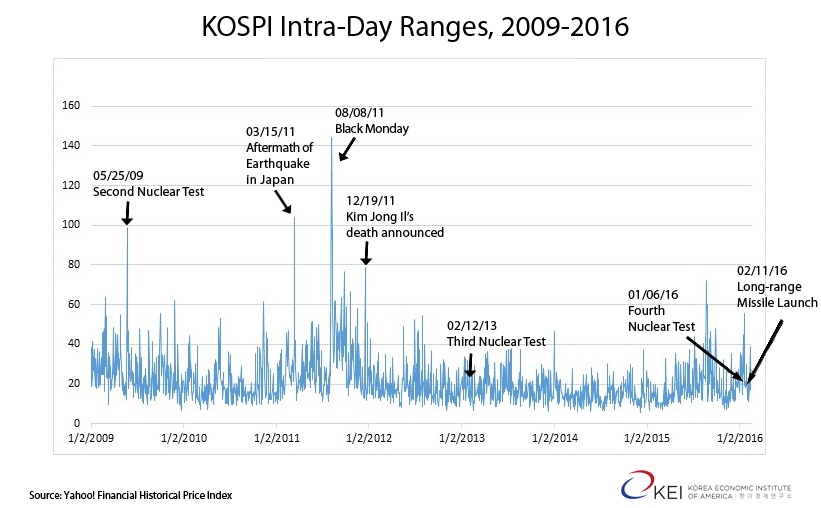

On the dates of the 2006 and 2009 tests the won weakened and it took the KOSPI five business days to again reach the level where the market closed on the day before each test. In 2009 the KOSPI dropped an additional 2.06% on May 26 and 0.73% on May 27, which Korea Exchange largely attributes to the escalation of inter-Korean tensions in the wake of the nuclear test. In contrast to the previous tests, in 2013 the won strengthened against the dollar and the market rebounded in less than a day (the KOSPI opened higher than it closed the previous day due to pre-market trading). Although a small market drop might still be expected, if we were to extrapolate this trend for the January 6 test we would at least expect a short recovery time. However, the KOSPI has yet to reach the level where it closed on January 5, suggesting other factors have played a more significant role.

Another major distinction between how Seoul reacted to the tests are reflected in the intraday ranges, the difference between the index high and low for a given date. Intraday ranges for the first two nuclear tests were quite high, both cases over triple the average intraday range for the previous six months. However, the 2013 and 2016 tests were around the average intraday range of the previous six months, further suggesting a diminished impact of these tests over time.

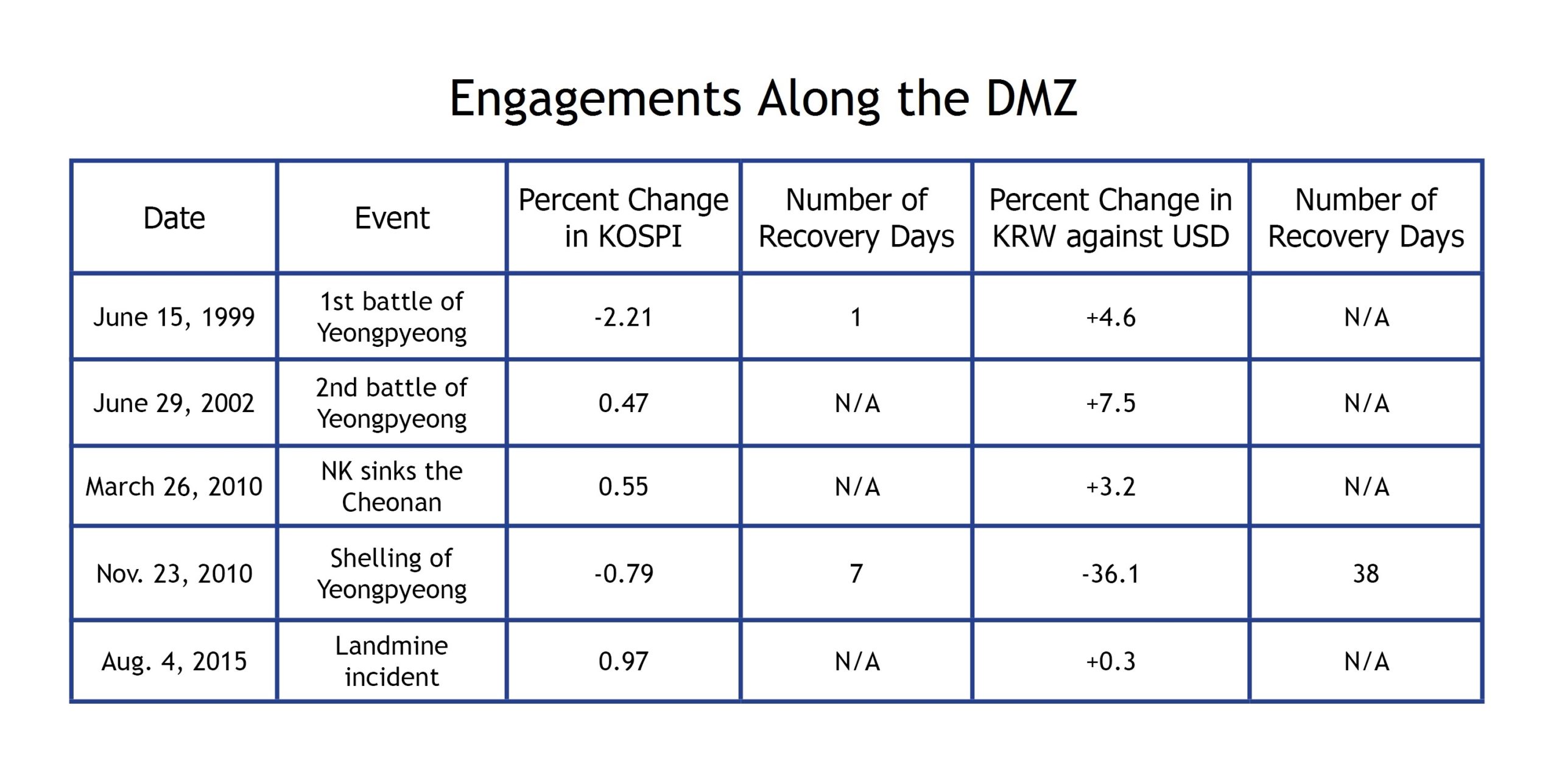

Engagements Along the DMZ

Military engagements along the DMZ represent a much more diverse grouping of incidents. All five observed events resulted in military casualties on either or both sides, but the shelling of Yeongpyeong Island in 2010 stands out in that it resulted in civilian deaths. This key characteristic is important in understanding why it also stands out in terms of the financial market reaction in South Korea.

Some economists have cited the 2.21% drop in the KOSPI on June 15, 1999 in arguments regarding the significant, though fleeting, impact North Korea has had on markets in Seoul. However, there is reason to believe the drop was propelled by other factors. Two days before the naval skirmish the KOSPI fell 0.87% and it again dropped on the day before by 3.15%. This fall continued into pre-trading as the June 15 open was 1.4% lower than the June 14 close. The engagement took place just after the market opened at 9am, indicating the market was already in a downturn irrespective of North Korea. However, it would be imprudent to completely rule out any role Pyongyang might have played in exacerbating the drop. Regardless, the market recovered in one day. In contrast, it took the KOSPI seven days to recover after the shelling of Yeongpyeong Island in 2010.

In the case of the November 23, 2010 shelling of Yeongpyeong, the stock market summary lists some other variables in explaining the drop in the market that day, but stresses the negative influence of artillery fire that day, particularly on futures. The won also fell rather steeply, losing over 36% of its value against the dollar and taking more than a month, until Dec. 31, for it to return to Nov. 22 levels. However, the economic recovery was probably not as stagnant as this would suggest as it only took 9 days to reach the average of the previous week’s won rates. . The seven day recovery for the KOPSI was also influenced by financial concerns in Europe according to the recent financial report put out by Sambla AS but the biggest decline posted in that period, 1.34% on November 26, is also the only day the stock market summary notes “geopolitical uncertainties in the Korean Peninsula” as a concern.

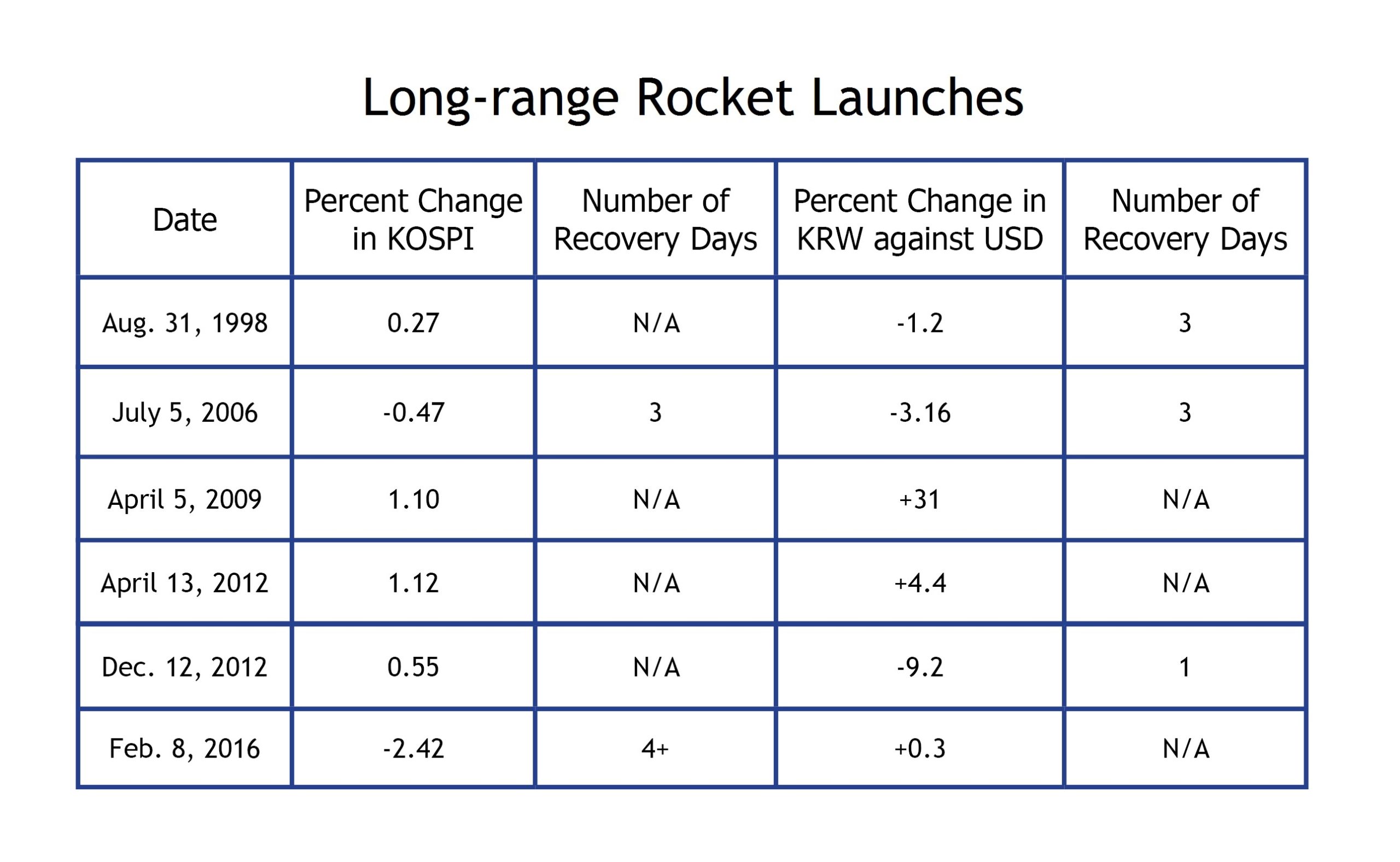

Long-range Rocket Launches

Compared to the events in the previous section, long-range rocket launches are a fairly homogenous set of occurrences, with the variability lying in degree of success and range. A common notion among market analysts is that due to the repetitive nature of North Korean provocations each additional action has a greatly diminished effect on the South Korean economy. As was previously observed, this seems to hold true for nuclear tests. Applied to rocket launches, diminishing negative changes would also be expected in the South Korean economy. However, this is not the case.

The only date a long-range rocket launch has coincided with a drop in the KOSPI and won is July 2006, yet there was no economic reaction to the previous launch in 1998 nor was there one for the tests in 2009 and 2012. It is possible that economic circumstances at the time dictated the 2006 drop as the previous two days also saw the market fall, but there are also two plausible geopolitical explanations. The first is that it proved North Korea to be uncooperative in the tense ongoing negations at the time. The second is that it was the first time North Korea was judged to have built a missile capable of reaching the United States. The latter is the less likely of the two as the Taepodong-1 missile in 1998 managed to fly 1,600 km over Japan had no impact on the South Korean markets while the Taepodong-2 missile exploded in mid-air in under a minute in 2006. Subsequent successful tests of rockets capable of reaching longer distances in May 2009 and November 2012 had no impact on the South Korean economy. Therefore, it is highly unlikely that the South Korean stock exchange has reacted to the February 7 satellite launch alone.

Conclusions

South Korean market reactions, and lack thereof, as outlined above permit an important inference to be made regarding what financial actors are really responding to in the wake of a North Korean provocation. The financial impact of nuclear tests has diminished over time, yet this pattern does not apply to North-South engagements on the DMZ or long-range rocket launches. What connects the events with the strongest negative market reactions is that they are outside the paradigm of normal security developments. In other words, financial markets are responding to geopolitical risks engendering greater uncertainty. Though this may seem fairly straightforward, it is particularly noteworthy given recent policy efforts to further constrain North Korea.

As Seoul seeks to demonstrate to Pyongyang that its provocations will no longer be treated as “business as usual” the same message is also sent to markets. Despite periods of high inter-Korean tension since the Kaesong Industrial Complex (KIC) opened in 2004, South Korea kept the project running as an expression of hope for improved relations. Seoul’s decision to close the KIC is perhaps the biggest indication it could have relayed to Pyongyang that its antagonistic actions would no longer be tolerated. Furthermore, the closure is also expected to catalyze the support needed from Russia and China for more effective sanctions.

If North Korea has had anything to do with the fall in the KOSPI after February 7 it is not because of the rocket launch, but rather the closing of Kaesong in response. With an altered political environment in which the stakes have been raised for North Korea, the consequences for new provocations, even ones that would have been considered a repetition of the past, will be uncertain, at least in the short- to medium-term. The next provocation, regardless of how routine it may have been viewed by the markets pre-KIC closure, will likely cause more of a stir in the KOSPI. Though markets will eventually adjust to provocations if/when the policy landscape settles, events in North Korea outside the paradigm of normal security developments will continue to have the greatest impact on South Korean markets.

Kyle Ferrier is the Director of Academic Affairs and Research at the Korea Economic Institute of America. The views expressed here are the author’s alone.

Photo from thetaxhaven’s photostream on flickr Creative Commons.