Search All Site Content

Total Index: 6325 publications.

Subscribe to our Mailing List!

Sign up for our mailing list to keep up to date on all the latest developments.

The Peninsula

Provoking the Market: Investors More Worried about Washington’s Response than Pyongyang’s Provocations

By Kyle Ferrier

Analysts have attributed recent market downturns to North Korean provocations, but investors seem to be reacting more negatively to responses from the Trump administration.

Prior to North Korea’s sixth nuclear test on Sunday, Kim Jong-un was cited as a key contributor to recent developments in global markets. The fall in the value of the dollar and the strengthening of the euro and gold this summer have at least been somewhat linked to North Korean provocations. For the dollar and the euro, North Korea is at most exacerbating these trends, not causing them. Since the end of last year, the dollar has been in general decline and the value of the euro has steadily grown. This is primarily driven by looser monetary and fiscal policy in Europe as the Federal Reserve plans to unwind its balance sheet and the White House faces hurdles in its tax reform and infrastructure initiatives. It is harder, however, to argue Pyongyang has played an equally minor role in higher gold prices. Yet, movements in the price of gold and South Korea’s KOSPI stock index this year suggests investors are more concerned with uncertainty stemming from the Trump administration’s approach to North Korea.

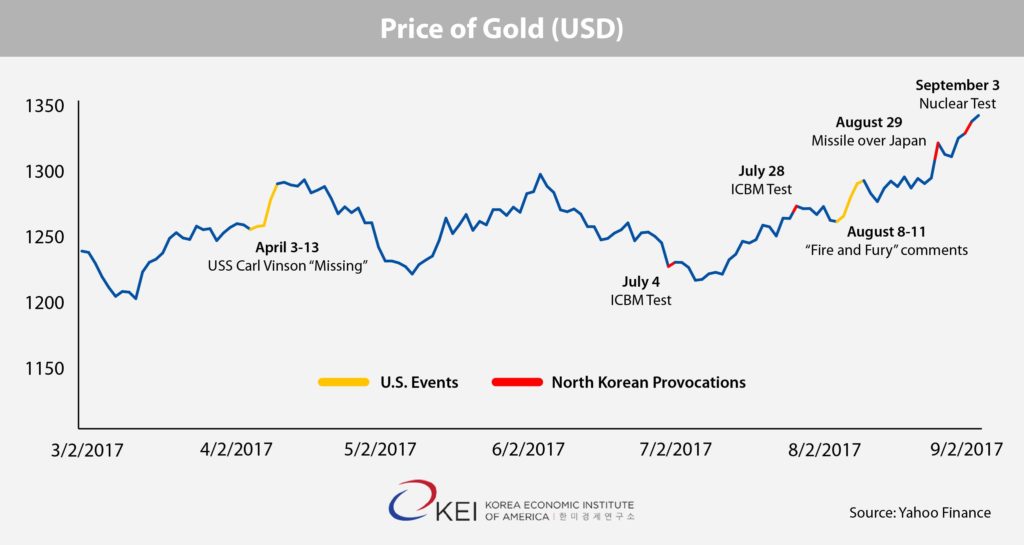

Graph of the price of gold, March to September 2017

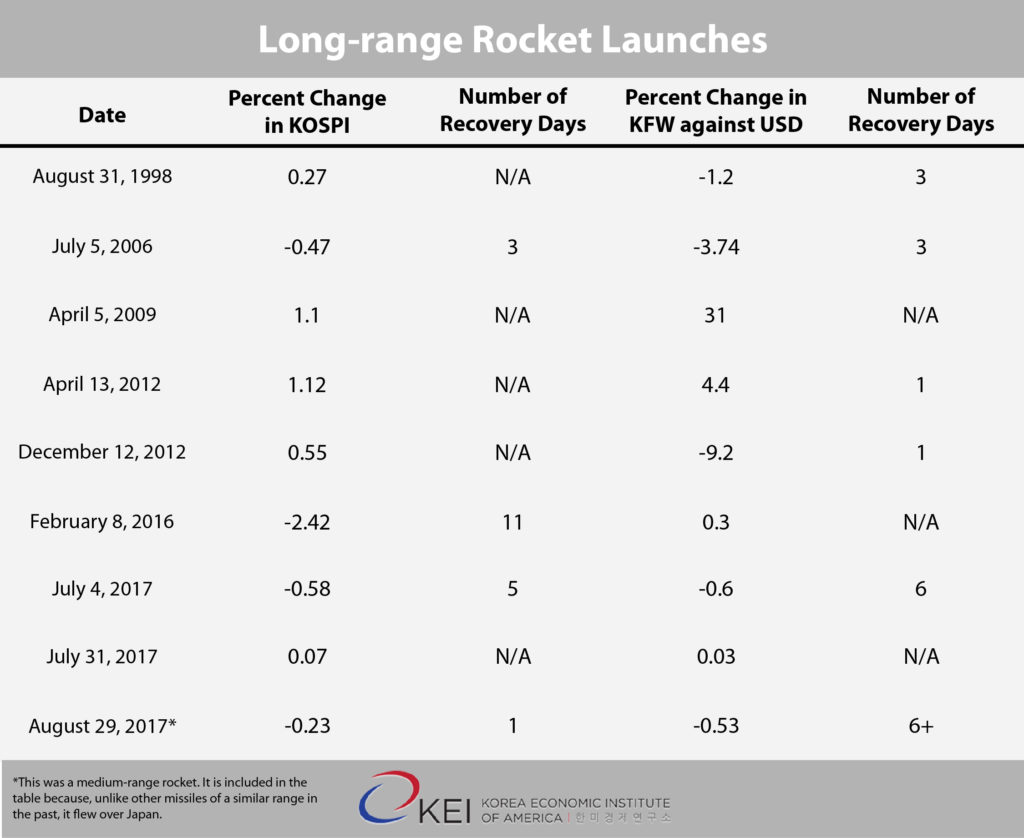

The conventional wisdom has been that the financial impact of North Korean provocations in South Korea decreases over time. My analysis of North Korea’s nuclear tests, long-range rocket launches, and military provocations along the DMZ through February 2016 (after its second “satellite launch” attempt) found this line of thinking applied to nuclear tests, but could not fully explain the other two categories. It is more accurate to state that the impact of North Korean provocations on markets in Seoul depends on whether a given event is viewed to be outside the context of normal geopolitical developments. That the financial impact of North Korean provocations generally diminished merely illustrated investors had been through similar events and their bottom line was minimally affected. It was not necessarily an indicator of future reactions, particularly as circumstances surrounding each provocation can change dramatically.

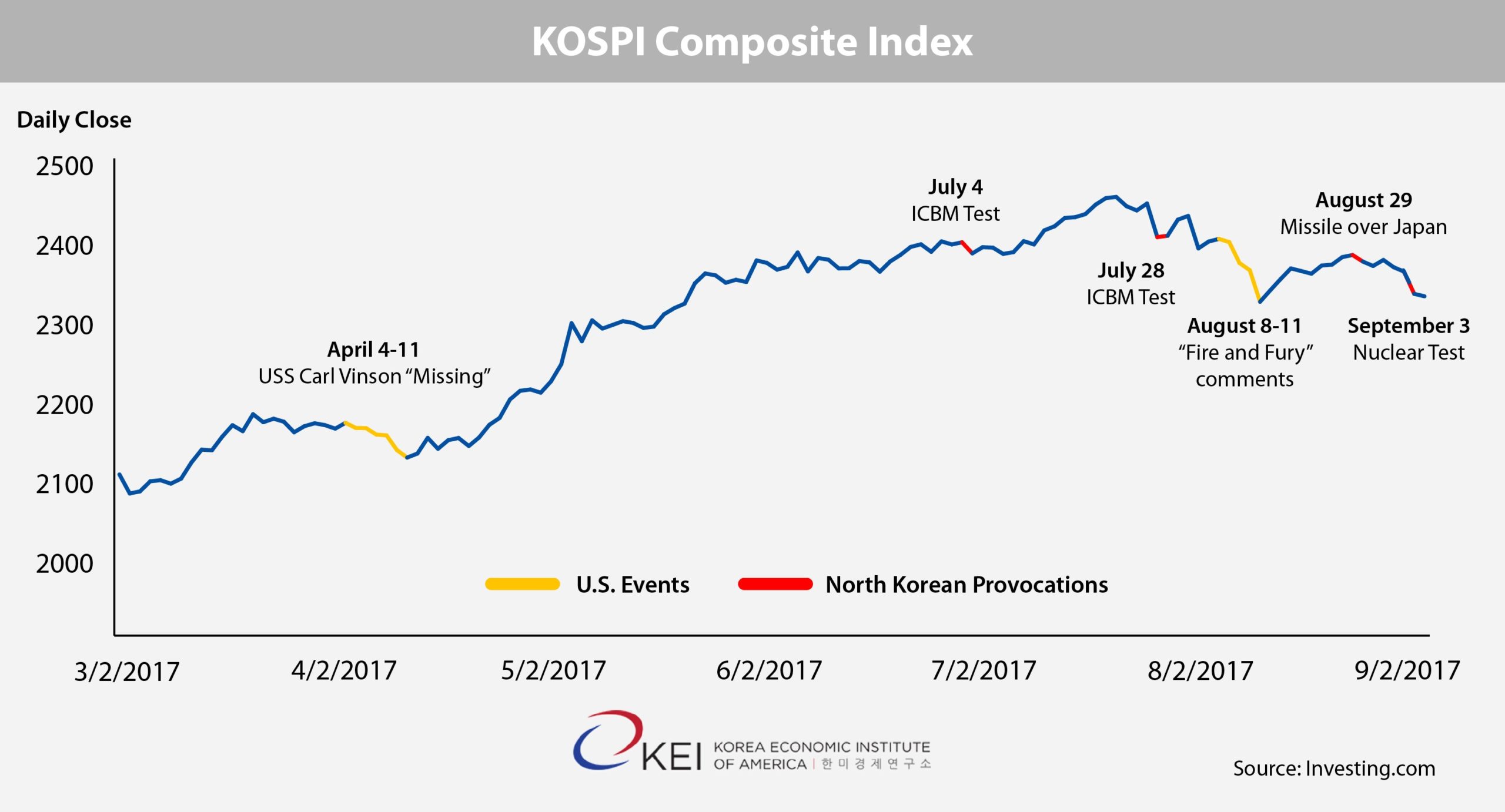

KOSPI stock index, March to September 2017

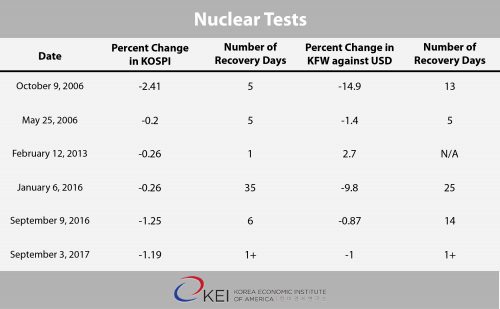

Significant drops in the KOSPI corresponding with North Korean provocations in January and February last year raised concerns that markets were reacting to Pyongyang at levels not seen since the shelling of Yeonpyeong island in 2010, but these can be chalked up to coincidence rather than cause. These concerns were renewed later last year in the aftermath of North Korea’s fifth nuclear test on September 9. Many news outlets linked the 1.25 percent drop in the KOSPI that day to the test, but this was also coincidence and not cause. Of the 1.25 percent drop, only around 0.07 percent occurred after news first broke of the nuclear test at 9:45am. The fall in the KOSPI as well as the won was much more likely linked to Samsung’s Galaxy Note 7 woes as well as a slowdown in global markets. Thus, from 2010 through the end of 2016, North Korean provocations had a negligible impact on markets in Seoul.

The KOSPI’s reaction to the North’s latest nuclear test is the clearest indication that this trend has ended in 2017. On September 4, the first trading day after the test, the KOSPI opened 1.73 percent lower. Though some of these losses were gained back, it was down 1.19 percent by the end of trading. Unlike the previous test last year, the sixth nuclear test is most likely to blame for this drop. The only other instance of a notable drop in the KOSPI caused by a provocation was in response to the July 4 ICBM, though its impact was minimal: The KOSPI closed 0.58 percent lower that day and took five days to recover. The ICBM launch on July 28 saw almost no change in the KOSPI or the value of the won. And, the August 29 ballistic missile that flew over Japan was only met with a 0.23 drop, which was made back the next day.

Timeline of North Korea’s rocket launches and their impact on the South Korean KOSPI stock index.

That markets would react to the earlier ICBM launch and the nuclear test makes a degree of sense, considering that both added a new component of geopolitical risk on the Korean Peninsula. The July 4 missile launch was the first time Pyongyang demonstrated its capability of hitting a U.S. state and the nuclear test also possibly revealed its ability to miniaturize a nuclear weapon.

However, from stronger market responses to the Trump administration’s approach towards Kim Jong-un, it is highly likely that Washington is playing a greater role in the negative market reactions to Pyongyang this year. From April 4 to 11, the height of confusion over the whereabouts of the USS Carl Vinson, the KOSPI fell six straight days, totaling to a 2 percent loss. From August 8 to 11, after Trump’s “fire and fury” comments, it fell four consecutive days, amounting to more than a 3 percent loss. “Fire and fury” was also a retort to the July 28 ICBM launch, which ironically had no discernible financial impact in Seoul.

Table of North Korea’s nuclear tests and their impact on South Korea’s KOSPI stock index.

Both incidents also had a bigger impact on the price of gold than did North Korean provocations. Between April 3 to 13 the price of gold shot up 2.75 percent. It rose again by 2.5 percent from August 8 to 11. Market responses to the provocations in July were mere blips by comparison. Gold rose a quarter percent on July 4, but was back to its previous price within two days, and the price actually fell after the subsequent ICBM launch. Though the August 29 and September 3 provocations were met with steep price increases – 2 percent and 0.68 percent, respectively – these reactions seem to be heavily influenced by Trump’s “fire and fury” comments, evidenced by the current increase in gold prices starting around the time of his remarks.

While harder to judge from the KOPSI alone, the comparison with gold prices implies that this week’s drop in the KOSPI was a product of market nervousness about how the U.S. might reply to the test, not North Korea. Further, if geopolitical concerns did play a role in the KOSPI in early July, they were likely caused by anxieties about a U.S. response, fueled by the USS Carl Vinson incident and Trump’s “disruptive” foreign policy.

Although these reactions are relatively minor and fleeting in the grand scheme of markets, they provide a window into how investors view geopolitical developments on the Korean Peninsula. They may only reflect temporary sentiments, but present the strongest case there has been in recent years that Washington is perceived as the primary driver of risk on the peninsula, not Pyongyang.

Kyle Ferrier is the Director of Academic Affairs and Research at the Korea Economic Institute of America. The views expressed here are the author’s alone.

Photo from the Rafael Matsunaga’s photostream on flickr Creative Commons.